Toast Inc (TOST) – Executive & Strategy Recap

In 2025, former President Trump’s proposed tax cut plan includes an intriguing provision:

It would exempt restaurant employees’ tips from income tax.

If this bill passes, the U.S. restaurant industry could truly enter a new “era of tipping.” Customers may become more proactive in leaving tips, and restaurants would need to accurately record, allocate, and report that flow. It’s not just about tax exemption—it could trigger a massive surge in demand for digitalized tip management systems.

But this raises a deeper question: Is a tip just a simple reward?

When we take a closer look at how American restaurants operate, tipping carries meanings far beyond money. Employees who interact directly with guests—the front-of-house servers—are typically the main recipients of tips. Meanwhile, back-of-house staff who prepare the meals often remain left out.

This imbalance continues to spark debate over wage disparities and fairness, even within the same team.

To address this issue, tip pooling has been gaining traction. Tip pooling refers to the practice of distributing all collected tips among staff according to predefined criteria. While it aims to promote fairness, it also requires carefully designed rules and transparent systems to avoid internal conflict.

This is exactly where TOAST comes into the spotlight.

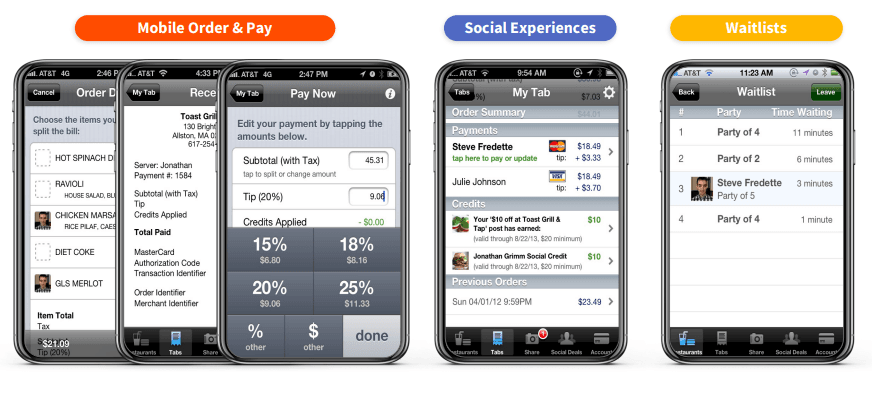

TOAST goes beyond being a simple Point-of-Sale (POS) terminal. It’s a cloud-based restaurant operating system that enables end-to-end management of tipping—from collecting tips to syncing with work hours, automated distribution, and tax reporting.

Today, a restaurant’s competitiveness depends not only on great food and service, but also on the fairness and intelligence of its operational systems.

The digital transformation of tipping is just beginning—and TOAST is positioning itself at the very heart of this shift.

👀 Why This Stock? (3-Point Summary)

1️⃣ The U.S. restaurant industry is undergoing a full digital transformation—from ordering and payment to staff management and marketing.

2️⃣ Toast is a restaurant operating system adopted by over 140,000 locations, evolving from a simple POS into an AI-powered integrated platform.

3️⃣ With a market penetration of just 15%, and still in the early stages of profitability and global expansion, Toast is worth watching from a long-term investment perspective.

1. Company Overview

Toast Inc. is a U.S.-based tech company that provides a cloud-based, all-in-one digital platform tailored for the restaurant industry. The company was founded in 2011 by three co-founders—Steve Fredette, Aman Narang, and Jonathan Grimm—in Boston, Massachusetts. In 2012, the company changed its original name from “Opti Systems” to “Toast Inc.”

Toast went public on the New York Stock Exchange (NYSE) on September 22, 2021, under the ticker symbol “TOST.” Since then, the company has rapidly expanded its footprint within the industry. The current CEO is Aman Narang, one of the original co-founders. Toast employs approximately 5,700 people globally, with its headquarters in Boston and additional operations in countries such as Ireland and India.

The company’s mission is “to empower the restaurant community to delight their guests, do what they love, and thrive.” Toast aims to go beyond being just a POS (Point of Sale) system. It offers an integrated platform—referred to as the “Restaurant OS”—that spans from front-end services like ordering and payments to back-office functions such as inventory and accounting management. This platform includes software, hardware, payment processing services, and a partner ecosystem, enabling restaurants to streamline their entire operation effectively.

2. Key Products and Services

As a platform company leading the digital transformation of the restaurant industry, Toast has built a comprehensive ecosystem that integrates software, hardware, payment infrastructure, and financial services. This section examines Toast's key products and services across four main pillars.

A. Software and SaaS Modules

a. POS Software

Toast provides a cloud-based POS (Point of Sale) application that supports order processing, menu and table management, and sales analytics. The software is deployed on tablets and mobile devices, and features a robust offline mode that allows transactions to continue even during internet outages.

b. SaaS Add-on Modules

In addition to its core POS system, Toast offers various add-on modules on a monthly subscription basis. These include online ordering and delivery integration, table reservations, customer loyalty programs, gift card issuance, employee scheduling, inventory management, and accounting integration.

These services enhance operational efficiency for restaurant clients and serve as a key driver of Toast’s ARR (Annual Recurring Revenue) growth.

c. Back-office Support Solutions

Toast also offers payroll and human resources management functions. These automate payroll calculations, tax filings, and tip distribution, reducing the administrative burden on operators.

In addition, Toast provides dashboards that visualize data such as sales, customer behavior, and cost analytics to offer business insights.

B. Hardware Portfolio

a. POS Terminals

Toast delivers hardware optimized for various restaurant environments. The Toast Flex terminal, for example, supports multiple configurations such as single-screen mode, kitchen displays, and customer-facing screens.

These devices are built with water-resistant and durable designs, and are easy to install and maintain on-site.

b. Payment Devices (Toast Tap)

Toast Tap is a wireless payment device that supports contactless transactions via Apple Pay, Google Pay, and tap-to-pay cards. It complies with PCI-DSS Level 1 security standards and integrates both in-store and online payments.

c. Peripheral Devices and Integrated Infrastructure

Through kiosks, Kitchen Display Systems (KDS), printers, and the Toast Hub, restaurants can build a fully integrated operational infrastructure.

Toast offers remote firmware upgrades and device monitoring to reduce the maintenance burden for clients.

C. Payment and Financial Services

a. Integrated Payment System

Toast processes various payment methods—credit cards, mobile payments, etc.—through its own payment gateway, ensuring secure transactions. Settlements are made daily, and transaction records and sales reports are seamlessly integrated into the POS system.

Toast’s mobile interface offers an intuitive user experience by combining order and payment processes, payment splitting among customers, and waitlist management. This enables flexible service for customers and efficient flow for operators.

b. Toast Capital (Lending Service)

Based on its proprietary transaction data, Toast offers small business loans to restaurants. Loan terms range from 90 to 360 days, and repayments are made as a fixed percentage of daily card sales—allowing for high repayment flexibility.

c. Partner Integration API

Toast supports broad integration with over 200 external partners (e.g., Uber, OpenTable, QuickBooks) via API connections. This allows client restaurants to connect their existing systems with Toast’s platform, increasing utility and creating a “lock-in” effect.

D. AI-Powered Smart Operations & Enterprise Solutions

a. ToastIQ Intelligence Engine

In May 2025, Toast launched ToastIQ, an AI-powered operational support engine. Key features include:

- Menu Upsells: Suggests additional items for staff to recommend to customers

- Digital Chits: Real-time updates on customer preferences or promotional events

- Shift at a Glance: Enables quick information sharing between shifts

- AI Marketing Assistant: Automated marketing tools powered by AI

- Ad Performance Visibility: Quantifies the effectiveness of marketing campaigns

These features automate daily operations and empower staff to deliver better service. By enabling data-driven and AI-informed decision-making, Toast moves beyond traditional POS systems into the realm of intelligent operational platforms.

b. Menu Price Monitor

Launched on May 13, 2025, the Menu Price Monitor tool tracks market price changes and helps restaurants adjust menu prices accordingly. This enables restaurants to implement competitive pricing strategies that enhance both profitability and customer satisfaction.

c. Enterprise-Grade Features for Large Chains

Toast offers customized services for complex, multi-location operations such as large restaurants and chain establishments.

As of 2025, this solution has been adopted by all Topgolf locations, select Applebee’s restaurants, and Beer on the Wall—a retail store managing over 10,000 products.

These businesses utilize Toast’s POS system, payment processing, kitchen displays (KDS), handheld devices, and centralized multi-location management tools to streamline their complex operations.

These examples highlight Toast’s capability to serve not just small independent restaurants, but also large-scale enterprises and chain brands through its versatile platform.

In summary, Toast’s key products and services form a comprehensive digital solution that spans software, hardware, payment systems, and financial services. This integrated portfolio positions Toast as a competitive platform capable of serving a wide range of clients—from small restaurants to large franchise operations.

3. Financial Performance

Since its founding, Toast has experienced rapid growth, culminating in its first-ever full-year GAAP profitability in 2024—a key turning point toward profitable expansion. As of Q1 2025, the company has demonstrated improvement across revenue, net income, EBITDA, and cash flow, clearly validating the scalability and stability of its recurring revenue model.

A. Annual Key Financial Metrics

a. Summary Table

The following table summarizes Toast’s core financial metrics from 2022 to 2024, including revenue, net income, EBITDA, GPV (Gross Payment Volume), and total location count.

Table 1. Toast Inc. Key Financial Metrics (2022–2024)

| Metric | FY2022 | FY2023 | FY2024 |

|---|---|---|---|

| Total Revenue | $2,731M | $3,865M | $4,960M |

| Net Income/Loss | -$275M | -$246M | $19M |

| Gross Profit | $511M | $834M | $1,190M |

| Adjusted EBITDA | -$115M | $61M | $373M |

| Total Locations | ~79,000 | ~106,349 | ~134,000 |

| GPV ($Billion) | $91.7B | $126.1B | $159.1B |

B. Store Count and ARR Growth

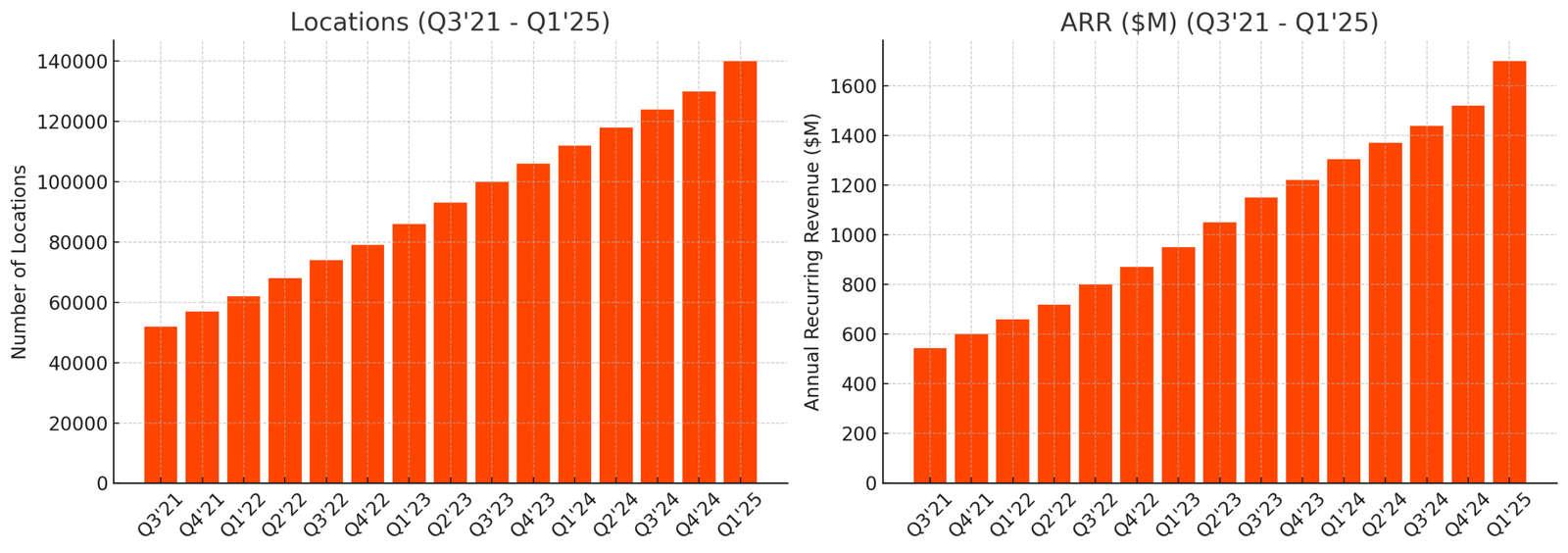

Toast has consistently expanded both its installed location base and ARR (Annual Recurring Revenue). As of Q1 2025, the company is estimated to operate approximately 140,000 locations, with ARR reaching around $1.7B—representing growth of +169% and +213%, respectively, compared to three years ago.

Figure 1. Growth of Locations and ARR (Q3'21 – Q1'25)

- Left Chart: Installed locations grew from 52K in Q3’21 to 140K in Q1’25

- Right Chart: ARR increased from $544M in Q3’21 to approximately $1.7B in Q1’25

C. Q1 2025 Results and FY 2025 Guidance

a. Q1 2025 Highlights

- Revenue: $1.34B (YoY +24.4%)

- Net Income: $56M

- Adjusted EBITDA: $133M (32% margin)

- Free Cash Flow (FCF): $69M

- New Locations Added: Over 6,000

b. Full-Year 2025 Guidance

| Metric | 2025 Outlook |

|---|---|

| Non-GAAP Subscription/Fintech Gross Profit | $1,745M – $1,765M |

| Adjusted EBITDA | $510M – $530M |

Management anticipates a record number of new store implementations starting in Q2 2025, and is targeting a full-year EBITDA margin of 30%.

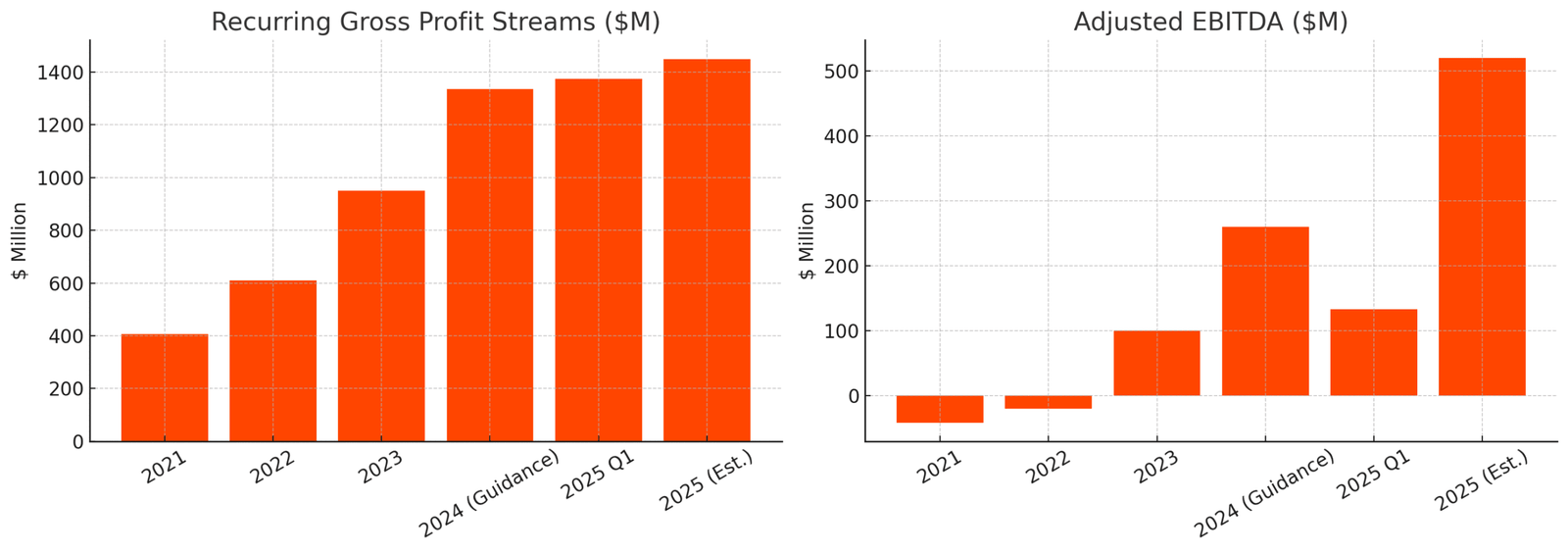

D. Recurring Revenue Profitability and EBITDA Trends

Toast’s revenue structure continues to shift from one-time transactions to a subscription-based recurring model. Correspondingly, Adjusted EBITDA has shown sharp improvement.

Figure 2. Recurring Gross Profit & Adjusted EBITDA Trends (2021–2025)

- Left Chart: Recurring gross profit rose from $406M in 2021 to an estimated $1,450M in 2025

- Right Chart: Adjusted EBITDA improved from –$42M in 2021 to a projected $520M in 2025

This trend demonstrates Toast’s ability to evolve from short-term revenue dependence to generating consistent cash flow and establishing a foundation for predictable long-term growth.

E. Overall Assessment

Toast reached a pivotal milestone in 2024 by achieving GAAP profitability. In 2025, the company continues to strengthen its position through recurring revenue expansion, growth in store count, rising EBITDA margins, and sustained FCF generation.

Investors increasingly assess Toast based not on short-term results but on its long-term ARR-driven growth potential and platform scalability. This strategic focus is central to justifying Toast’s valuation as a high-growth SaaS-plus-fintech enterprise.

4. Strategic Summary: Long-Term & Dollar-Cost Averaging Perspective

A. Why Consider This Stock for Long-Term Investment

Toast is evolving beyond a simple POS system to become a fully integrated "Restaurant Operating OS" that digitizes every aspect of restaurant operations.

The U.S. foodservice industry still has relatively low digital penetration. Toast currently captures only about 15% of the total addressable market (TAM), leaving substantial room for expansion. Following its first GAAP profit in 2024, Toast has entered a structural turning point where both profitability and growth are now being achieved—marking its transition into a high-growth SaaS + fintech platform.

ARPU (Average Revenue Per User) is structurally improving, driven by AI-powered solutions, a partner ecosystem, and hardware-based lock-in strategies. Toast is also expanding its target market from small restaurants to large chains.

For these reasons, Toast is a promising long-term play, benefiting from the broader trend of digital transformation and poised to redefine the operational standard in the restaurant industry.

B. Economic Moat Assessment

a. Types of Moats

- ✅ Intangible Assets: Toast has secured brand trust through partnerships with Michelin-rated restaurants and Topgolf.

- ✅ Network Effects: Data from over 140,000 locations enhances AI functionality. As more users join, recommendations and operational efficiency improve.

- ✅ Switching Costs: The integrated hardware-software system and tailored setups create significant friction in switching. Customer churn is under 1%.

- ✅ Economies of Scale: With $900M in cash and over $150B in GPV, Toast is continuously improving operational efficiency and data utilization.

- ✅ Efficient Scale: Few competitors in the U.S. market offer a fully integrated restaurant platform, and Toast stands out for its technical and service sophistication.

b. Moat Rating: Mid-Level to Wide Moat

c. Summary of Evaluation

Toast is a platform company with a hybrid moat built primarily around switching costs and data-driven network effects.

Its hardware-software integration, POS lock-in effects, and low churn rate (under 1%) create a robust switching cost moat. AI capabilities such as ToastIQ and Menu Monitor, fueled by massive transaction data from 140,000+ locations, strengthen the company’s network effects.

In terms of intangible assets, partnerships with premium restaurants have increased brand recognition, though industry-standard barriers are still developing.

Economies of scale are now forming, with recurring revenue (ARR) surpassing $1.7B and GPV exceeding $150B, indicating entry into a stabilization phase.

Efficient scale is somewhat limited by the fragmented nature of the U.S. POS market, but Toast’s technological sophistication and integrated platform strategy give it a competitive edge.

Overall, Toast is currently transitioning from a Mid-Level to a Wide Moat business model.

d. Key Conditions for Strengthening Moat (Mid-Level → Wide)

| Moat Type | Strengthening Condition |

|---|---|

| Switching Costs | Deepen customer dependence by offering integrated accounting/CRM solutions for enterprise chains |

| Network Effects | Extend AI capabilities to external restaurant ecosystems (e.g., reservations, reviews, menu APIs) |

| Intangible Assets | Enhance industry perception through U.S. foodservice certification or Toast Certified labeling |

| Efficient Scale | Increase structural defensibility by acquiring and consolidating competitors in niche segments |

C. Key Metrics Summary

- Revenue CAGR +35% (2022–2024): Toast grew at an average of 35% annually, rapidly gaining market share in the restaurant POS space.

- First GAAP profit in 2024: Toast shifted from three years of consecutive losses (2021–2023) to sustainable profitability.

- Adjusted EBITDA: $373M → $530M (2025 guidance): The company is achieving “efficient growth” by managing fixed costs effectively.

- Forward PER ~40–50x (2025F): While high in the short term, its SaaS+fintech hybrid model justifies a structural premium based on ARR growth and TAM expansion.

- FCF Margin: 5.1% (Q1 2025): Reduced hardware subsidies and operating leverage are driving positive cash flow.

- ROE: 5–7% range: With profitability returning, capital efficiency is improving and expected to rise further as the platform matures.

- NRR (Net Revenue Retention): 111%: Existing customers are actively adopting additional services, reinforcing strong lock-in effects.

- Cash Reserve: ~$900M / Very Low Debt: Toast maintains a stable financial structure that supports both growth and investment capacity.

D. Role in a Portfolio

- Stock Nature: SaaS + fintech hybrid platform benefiting from restaurant industry digitalization

- Investment Role: A high-growth platform company with structural entry barriers in a fast-growing sector

- Investment Approach: Given its still-low market penetration, a dollar-cost averaging strategy aligned with TAM expansion and profitability gains is effective. Investors should monitor global expansion, AI rollout, ARR trends, and customer growth each quarter to adjust weighting accordingly.

E. My Perspective & Interpretation

I view Toast not as a mere POS hardware provider, but as a SaaS-based infrastructure platform reshaping the restaurant industry.

The U.S. foodservice sector remains digitally underpenetrated, and Toast is at the heart of that transition. Following GAAP profitability in 2024, the company has begun benefiting from operational leverage. Meanwhile, AI-powered solutions like ToastIQ clearly differentiate the platform from its competitors.

Though global expansion is still in its early stages and carries certain risks, the simultaneous progress in TAM growth and profitability signals a compelling long-term opportunity for investors.

For these reasons, I classify Toast as a stock better evaluated by its future dominance than by current earnings—a growth stock suitable for long-term, gradual accumulation.

5. Competitive Advantages

Toast has evolved beyond a mere POS hardware provider to become a SaaS + fintech platform that digitizes the full spectrum of restaurant operations. As of 2025, Toast’s key competitive strengths lie in its technological innovation, strong customer lock-in, integrated ecosystem, proprietary data assets, and regulatory readiness—creating economic moats that are difficult for latecomers to replicate.

A. Market Share and Industry Positioning

a. Location Penetration and Transaction Share

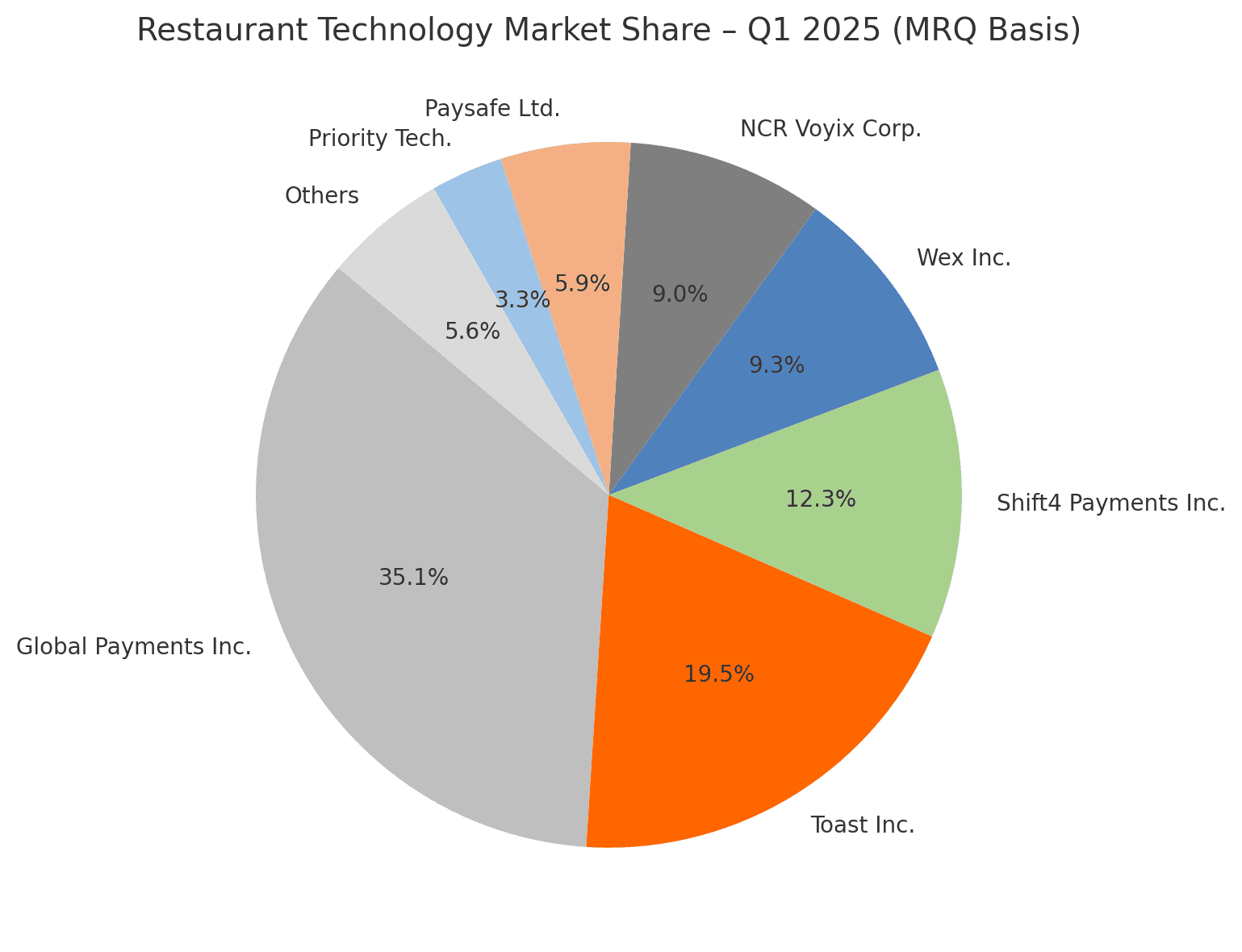

As of Q1 2025, Toast is deployed in approximately 140,000 restaurant locations across the U.S., representing about 18–20% of all foodservice establishments. In terms of card payment volume, Toast commands a 19.5% market share—outpacing competitors like NCR Aloha (16%) and Clover (8%).

b. Visualized Market Share

Source: CSIMarket

Source: CSIMarket

According to 2025 Q1 Restaurant Technology Market Share data, Toast holds the highest share among tech-driven independent vendors, ahead of Shift4 (12.3%), Wex (9.3%), and NCR Voyix (9.0%).

c. Strategic Implications

The CEO of Toast emphasized that the platform’s penetration in the U.S. market remains at just 14–18%, signaling substantial headroom for growth. The company’s strategy of targeting local restaurants, emerging brands, and digitally underserved operators continues to support its rising market share.

B. Technological Capabilities and Product Sophistication

a. Cloud-Based Integrated POS Architecture

Toast’s Android-based cloud platform supports real-time updates, remote management, and uninterrupted maintenance. Compared to legacy on-premise systems like NCR and Micros, Toast offers superior scalability and lower maintenance costs.

b. AI-Driven Operational Automation

Launched in 2025, ToastIQ automates upselling, shift summaries, and personalized recommendations using AI. Meanwhile, Menu Price Monitor analyzes competitor pricing trends and helps restaurants optimize their pricing strategies in real-time. These capabilities reduce operator dependency and directly increase revenue per customer.

C. Lock-In Structure and Ecosystem Strategy

a. Integrated Ecosystem and Feature Scalability

Toast unifies all key functions—POS, online ordering, delivery, reservations, payroll, accounting, lending—under one account. Its 200+ API integrations with partners such as Uber, QuickBooks, and OpenTable maximize flexibility and ecosystem scalability.

b. Customer Retention and NRR

In 2023, Toast’s Net Revenue Retention (NRR) stood at 111%, with a churn rate under 1%. This indicates not only high retention but also ongoing upsell adoption and consistent ARPU growth over time.

c. Hardware-Based Lock-In

Toast supplies proprietary POS terminals, kitchen display systems (KDS), kiosks, and handheld devices, all tightly integrated with its software. These hardware products are not easily compatible with other platforms and require significant time and cost to replace and retrain staff.

Initially offered below cost to drive adoption, Toast shifted in 2024 to reduce subsidies and improve margins—thereby increasing customer switching costs over time. This combination of physical and financial lock-in forms a substantial retention barrier beyond mere customer satisfaction.

D. Brand Trust and Data-Driven Advantage

a. Premium Brand Partnerships

Toast partners with one-third of James Beard Award-winning restaurants and over half of Michelin-starred establishments. It also serves major chains like Applebee’s and Topgolf. These high-profile associations position Toast as a preferred brand among new restaurateurs and those upgrading their systems.

b. Data Asset-Driven AI Capabilities

Toast has accumulated hundreds of billions of dollars in payment and operational data. This fuels features like personalized AI recommendations, performance benchmarking, and automated menu optimization. These data-driven tools enhance both operational efficiency and platform dependency.

E. Regulatory Readiness and Infrastructure Reliability

a. Compliance and Financial Services Resilience

Toast maintains PCI-DSS Level 1 certification and shares the risk of its financial products (e.g., Toast Capital) through partnerships with external lenders. For example, in 2023, Toast swiftly rolled back its online order fee policy in response to public and regulatory pressure, showing its agile compliance strategy.

b. Infrastructure Reliability

Toast ensures 99.99% uptime via its proprietary cloud infrastructure, offline transaction mode, and remote monitoring systems. This dramatically reduces the risk of service disruption and strengthens long-term customer trust.

6. Risk Factors

A. Regulatory and Legal Risks

a. Payment and Data Regulation

Toast is exposed to multiple regulatory frameworks, including credit card fee structures, data privacy laws (such as CCPA), and data storage/processing requirements. Stricter regulations could reduce payment profitability or result in fines, and data breaches could lead to significant reputational damage.

b. Financial Services and Lending Regulations

Toast Capital offers small business loans to restaurants, subjecting the company to lending laws, consumer protection regulations, and interest rate caps. In an economic downturn, rising default rates could trigger regulatory scrutiny and an increase in non-performing assets.

c. Labor Law and State Tax Compliance

Toast’s HR solutions, including Toast Payroll, must be continuously updated to comply with state labor laws and tax codes. Noncompliance could lead to legal disputes or service disruptions.

B. Competitive Pressure and Growth Slowdown Risks

a. Increased Penetration by Competitors

Rivals such as Clover, Square, TouchBistro, and SpotOn are rapidly expanding feature sets and aggressively targeting Toast’s core market of small and independent restaurants. Notably, Clover already serves over 160,000 restaurant clients—potentially surpassing Toast in customer base.

b. Price Competition and Margin Compression

Intensifying competition could drive down payment processing fees and force Toast to offer free hardware or discounted software subscriptions. Toast has historically sold hardware below cost, which, if continued, could negatively affect gross margins.

c. Market Saturation and Limited New Growth

As of 2025, Toast covers roughly 18–19% of independent U.S. restaurants—a relatively high penetration rate. Once market share reaches a saturation point, acquiring new customers becomes more difficult, potentially slowing growth.

C. Profitability, Cash Flow, and Operational Risks

a. Low Margin Structure and GPV Sensitivity

Toast’s core revenue stream—payment processing—is a low-margin business. As of 2024, its gross profit margin stood at just 21.7%. Economic downturns or weather disruptions that reduce restaurant activity could lead to a sharp decline in GPV and profitability.

b. Hardware Losses and Lock-In Strategy Costs

Toast has used below-cost hardware pricing to drive customer lock-in, resulting in a $170M hardware loss in 2023. Considering hardware replacement and upgrade cycles, this strategy could weigh on short-term profitability.

c. Continuous Investment Costs and Capital Outflows

Toast is actively investing in R&D, international expansion, and customer acquisition. It also plans stock buybacks, which will lead to additional cash outflows. While the company ended 2024 with $903M in cash, its 12-month CAC payback period makes cash flow management a critical task.

D. Macroeconomic and Industry Risks

a. Restaurant Industry Cyclicality

Toast’s core clientele—the restaurant industry—is highly sensitive to economic cycles. Slowdowns in consumer spending or inflation spikes can directly impact revenues. External shocks such as pandemics or natural disasters could increase restaurant closure rates.

b. Potential Failure in Global Expansion

Toast has entered select international markets such as Canada, but cultural differences, local regulations, and competitive pressures could limit success. Outside the U.S., maintaining high fee structures is difficult, and overseas M&A carries additional risk.

c. Technological Disruption and Talent Loss

If Toast fails to adapt to emerging technologies such as AI, robotics, or blockchain-based payments, its competitive edge could erode. Post-restructuring cultural instability and the potential loss of key talent also remain ongoing risks.

7. Future Outlook and Strategic Vision

A. TAM (Total Addressable Market) Expansion Strategy

a. Expanding TAM in the U.S. and Globally

As of now, Toast serves around 140,000 restaurants out of an estimated 875,000 in the U.S., representing a market penetration rate of just 15–16%. This means that over 85% of the domestic market remains untapped.

Looking globally, there are approximately 280,000 restaurants in countries like Canada, the UK, and Ireland. Excluding China, global estimates suggest up to 15 million foodservice businesses could be included in Toast’s long-term TAM. Toast already supports approximately 2,000 international locations, and its ARPU (Average Revenue Per User) is increasing rapidly—indicating early global expansion success.

b. Structural Growth in the Global POS Market

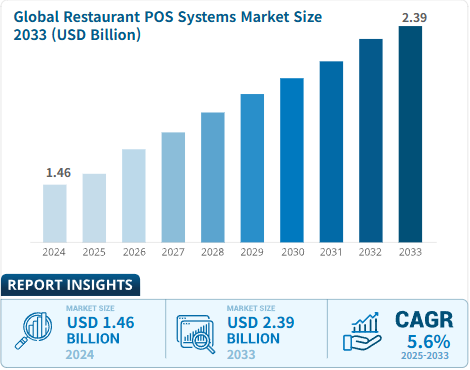

The restaurant POS systems market was valued at approximately $1.46B in 2024 and is projected to grow at a CAGR of 5.6% through 2033, reaching an estimated $2.39B. Rising demand for cloud-based POS, integrated payments, and AI-powered operational tools aligns directly with Toast’s strengths, positioning the company to benefit from this expanding market.

c. TAM Diversification via New Markets & Products

Toast is expanding its TAM beyond traditional restaurants into food & beverage retail—including beer cafés, bakeries, and bars—by enhancing inventory and ordering integration capabilities.

In the enterprise segment, Toast is targeting high-value verticals through multi-location management features (above-store suite) and has secured large clients such as Applebee’s, Topgolf, and Perkins. These strategies illustrate that Toast is not only growing its share within existing markets but is also actively broadening its TAM base.

TAM-focused expansion highlights Toast’s long-term structural growth potential beyond short-term earnings metrics.

B. Market Trends and Strategic Positioning

a. Accelerating Digitalization in Foodservice

There’s a surge in demand for digital technologies such as self-order kiosks, smart scheduling, and automated kitchen displays. The market is increasingly favoring platforms that integrate POS, delivery, inventory, and loyalty systems—a trend that aligns perfectly with Toast’s all-in-one solution approach.

There’s a surge in demand for digital technologies such as self-order kiosks, smart scheduling, and automated kitchen displays. The market is increasingly favoring platforms that integrate POS, delivery, inventory, and loyalty systems—a trend that aligns perfectly with Toast’s all-in-one solution approach.

b. AI and Voice-Based Operational Efficiency

AI is being rapidly adopted in customer service chatbots, sales forecasting, and smart reordering. Toast’s product roadmap actively reflects this shift, and as AI implementations begin showing financial impact in 2025, analysts are taking note of Toast’s innovation leadership.

c. Integration of ToastIQ and AI Capabilities

In May 2025, Toast launched ToastIQ, an AI engine that includes tools like the menu optimization assistant "Sous Chef", generative AI for marketing, and workflow automation. With data from over 140,000 restaurants, ToastIQ analyzes customer behavior and sales patterns, improving operational efficiency, customer experience, and revenue.

d. Personalization and Sustainability Trends

ESG-aligned technologies such as energy-efficient kitchens and waste reduction systems are gaining traction. Simultaneously, personalized menus, allergy filtering, and loyalty-driven promotions are driving more customized customer experiences.

C. Profitability-Focused Management Strategy

a. Cost Efficiency and Operating Leverage

Since 2024, Toast has embraced “Efficient Growth” as a key initiative—cutting operating expenses and optimizing labor costs. As a result, its profitability metrics, including adjusted EBITDA, have improved even as revenue continues to grow, prompting upward revisions to its full-year guidance.

b. Enhancing Shareholder Value and Financial Resilience

In 2024, Toast executed a $250M share buyback program to stabilize share price and strengthen investor confidence. Looking ahead, the company is committed to balancing growth investments with profitability, prioritizing R&D and AI technology development.

D. Analyst and Expert Evaluations

a. Wall Street Analyst Perspectives

Out of 24 analysts, 12 rate Toast as a “Buy” and 12 as “Hold,” with an average price target of $41.21. While many view Toast’s ARR growth and TAM expansion positively, there are concerns regarding valuation levels and long-term profitability.

b. Forward Outlook and Financial Guidance

Toast’s management has provided 2025 full-year guidance of $1.775B–$1.795B in gross profit and $540M–$560M in adjusted EBITDA. Following the company’s first GAAP profit in 2024, improvements in operating leverage and margin expansion are driving sustained profitability.

c. Risk Monitoring by Analysts

Ongoing challenges include competitive pressure, high customer acquisition costs, and macroeconomic risks. Analysts are closely monitoring Toast’s ability to manage these risks while maintaining its high-growth business model.

8. Appendix: Trump’s Second-Term Tax Proposal and Toast’s Tip Management Differentiation

In 2025, President Trump’s second administration is advancing a new tax reform proposal that includes income tax exemptions for tips. If enacted into law, this provision is expected to reshape the U.S. foodservice industry by significantly elevating the importance of tip management. For restaurants, this isn’t just about customers leaving larger tips—it becomes essential to have a system that accurately tracks, fairly distributes, and transparently reports tip income for tax compliance and operational efficiency.

Labor compensation structures in the U.S. restaurant industry are heavily tip-based. However, there are persistent equity issues between front-of-house staff (servers), who receive most tips, and back-of-house staff (kitchen workers), who are often excluded. As a result, “tip pooling”—a system to fairly distribute tips among all employees—is gaining attention. Proper implementation of tip pooling requires precise time tracking, clear allocation rules, and automated distribution systems.

This is precisely where Toast’s competitive edge shines. Toast offers a cloud-based tip management solution that goes beyond a traditional POS (Point-of-Sale) system. It enables restaurants to manage the entire lifecycle of tips—from collection to time-based allocation, automated distribution, and tax reporting—within a single integrated platform. In an era where digital transformation of tip management is accelerating, this functionality enhances both operational efficiency and employee trust.

Considering both the risks and opportunities tied to potential policy changes, Toast is emerging as a trusted platform that enables restaurants to adapt quickly and reliably to evolving tip-related regulations. In the short term, this supports regulatory compliance; in the long term, it contributes to sustainable competitive advantage through improved employee satisfaction and streamlined operations.

9. Two-Minute Pitch

Peter Lynch emphasized the importance of being able to deliver a two-minute pitch about a stock you are interested in, including the reasons for buying it, the company’s prospects, and its story. If you have thoroughly researched and can confidently articulate this two-minute pitch, you may consider purchasing the stock.

(Note: All investment decisions and responsibilities rest solely with you. Always invest with surplus funds and focus on long-term investments.)

Toast, Inc. has established a distinctive market position through its cloud-based technology platform specialized for the restaurant industry. More than just a POS provider, Toast delivers an all-in-one system that integrates ordering, payment, inventory, marketing, and HR management—offering tangible operational improvements across a wide range of restaurant clients. Over the past three years, the company has demonstrated steady growth in revenue, transaction volume, and total customer locations. In particular, achieving its first full-year GAAP profit in 2024 marked a key turning point, proving Toast’s ability to pair rapid top-line growth with improving profitability.

Toast’s differentiated competitiveness lies in product innovation powered by AI and its restaurant-specific functionality. Solutions like ToastIQ and Menu Price Monitor support operational automation and data-driven decision-making, reinforcing customer lock-in while building a moat that is difficult for competitors to replicate. The successful acquisition of enterprise clients such as Applebee’s and Topgolf also validates Toast’s ability to scale its platform from small businesses to large chains, highlighting its flexibility and scalability.

Nonetheless, Toast faces several challenges, including intensifying competition, regulatory shifts, and technology-related risks. Issues such as data security, responsible use of AI, reliance on third-party cloud infrastructure, and hardware-related losses must be closely managed. Moreover, customer acquisition costs and early-stage hurdles in global expansion—such as cultural and legal complexities—require strategic attention.

Despite these headwinds, Toast occupies only a small fraction of the overall restaurant tech market, indicating substantial room for TAM (Total Addressable Market) expansion. The company’s profitability trajectory is clear, and with a strong leadership roadmap, product sophistication strategy, and a loyal customer base, Toast is well positioned to become a central player in the evolving restaurant technology ecosystem.

In summary, Toast is no longer just a POS provider—it is evolving into an intelligent partner that leads the digital transformation of the foodservice industry. Backed by robust technology and a competitive platform, Toast is viewed as a high-potential company poised for sustained growth.