👀 Why This Company? (3‑line Summary)

1️⃣ Rising U.S. debt, soaring delinquency rates, student loan policy changes, and the Trump administration’s reforms have intensified credit risk, creating strong demand for advanced risk management and decision systems among financial institutions.

2️⃣ In this environment, FICO’s ubiquitous FICO Score and intelligent decision-making platform have positioned the company as a cornerstone of U.S. financial infrastructure.

3️⃣ With continuous shocks to credit conditions and a broader digital shift, FICO—as a provider of “decision infrastructure”—warrants renewed consideration for long-term investment.

Executive Summary – FICO (Fair Isaac Corporation)

1. Company Overview

-

Founded in 1956 by Bill Fair and Earl Isaac; now operates in 25+ countries.

-

Pioneer of the modern credit scoring system, with deep integration in U.S. financial infrastructure.

-

Dual-business model structured around credit scoring (Scores) and enterprise decision automation (Software).

2. Key Products & Services

-

Scores Segment:

-

FICO® Score is used by 90%+ of U.S. lenders and powers ~90% of U.S. mortgage originations.

-

Platform-based royalty model via Experian, Equifax, and TransUnion.

-

myFICO.com offers consumer-facing credit tools and subscriptions.

-

-

Software Segment:

-

FICO Platform delivers AI-driven decision automation across fraud, customer management, and compliance.

-

Key solutions include Falcon Fraud Manager, Blaze Advisor, and decision optimization tools.

-

ARR growth of 31% YoY (FY2024) with DBNRR of 123%.

Image Description:

This infographic visualizes the revenue model of FICO's credit scoring business.- FICO develops the credit scoring algorithm.

- It licenses the algorithm to credit bureaus such as Experian, Equifax, and TransUnion.

- Lenders—banks, credit card companies, and loan providers—use the score to evaluate consumer creditworthiness.

- Consumers indirectly pay for the use of the score through loan-related fees.

💰 Revenue Flow Summary:

Consumer → Lender ↔ Credit Bureau → FICO

(Indirect Fee → Score Access Fee → License Royalty)

3. Financial Performance

-

FY2024 Revenue: $1.72B (+13% YoY); Net Income: $513M (+19% YoY); EPS: $20.77 (+23% YoY).

-

EBITDA margin: 45%; Free Cash Flow margin: ~35%; ROIC: 45.43%.

-

Scores segment operating margin: 88%, driving overall profitability.

-

Projected FY2025: $1.98B revenue and $624M net income.

4. Competitive Advantages

-

De facto industry standard in U.S. credit scoring with high switching costs.

-

Strong pricing power due to embedded infrastructure role and low per-loan score cost.

-

Proprietary data and patented algorithms fuel predictive modeling leadership.

-

“Augmented Intelligence” approach enhances AI trust and regulatory alignment.

-

Wide Moat across intangible assets, switching costs, and efficient scale.

5. Risk Factors

-

Rising competition from VantageScore (FHFA-approved from 2025) and alternative credit models.

-

Exposure to regulatory scrutiny (DOJ antitrust suits, data privacy risks).

-

Customer concentration: ~91% revenue from financial services; ~84% from North America.

-

Potential channel risk from credit bureau partners who also promote competing models.

6. Future Vision & Outlook

-

Strategic shift toward intelligent enterprise via FICO Platform.

-

“Land and Expand” cloud strategy fueling revenue per client and NRR growth.

-

Expanding partner ecosystem (e.g., AWS, TCS) and API marketplace.

-

Global market tailwinds:

-

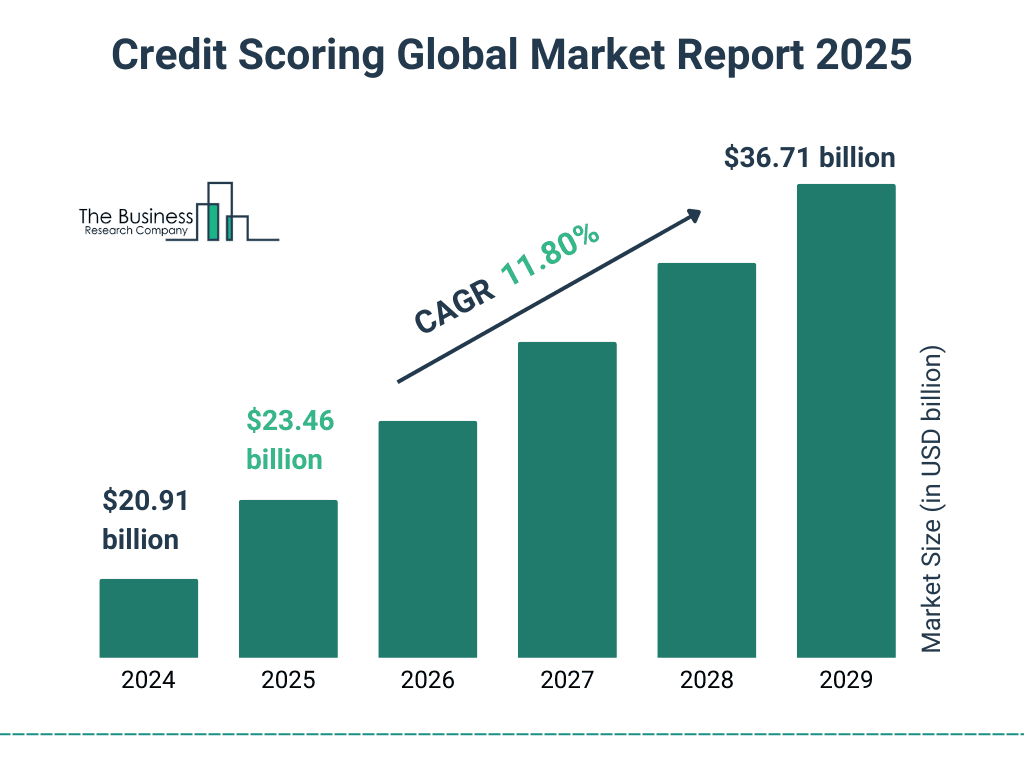

Credit scoring market CAGR 11.8% (2024–2029)

-

Fraud & risk analytics CAGR 18.2% (2024–2034)

-

-

FY2025 guidance: >15% revenue growth, 25% non-GAAP EPS growth.

-

Analysts maintain “Strong Buy” to “Moderate Buy” outlook.

Why FICO Fits a Long-Term Portfolio: Strategy Summary

-

Stock Profile: Global leader in credit scoring and AI-powered decision software

-

Investment Role: High-margin infrastructure play with deep financial system embedment

-

Approach Strategy: Long-term DCA entry focused on platform migration and ARR growth

-

Moat Evaluation: Wide Moat — based on regulatory lock-in, switching costs, and proprietary data

🔹 Supporting Points:

-

1️⃣ Business Model Resilience: Dual revenue streams (royalty + SaaS) offer stability and scalability.

-

2️⃣ Moat Strength: FICO Score deeply embedded in 90%+ of U.S. financial institutions; hard to replace.

-

3️⃣ Financial Quality: 45% EBITDA margin, 45.4% ROIC, and >$600M annual FCF.

-

4️⃣ Growth Levers: Platform expansion, cross-sell via “Land and Expand,” and partner integrations (AWS, TCS).

-

5️⃣ Portfolio Fit: Ideal for long-term investors seeking exposure to fintech infrastructure with AI leverage.

-

If you're interested in the full article on Fico Issac Corporation(FICO), click here.