Fair Isaac Corporation (FICO) – Executive & Strategy Recap

During the 2008 global financial crisis, even individuals with “high credit” scores above 720 faced default. Delinquency rates, once nearly 0%, surged to over 5%, exposing fatal flaws in the credit scoring system. The crisis was not limited to subprime borrowers—it spread across the middle class, high-credit individuals, and financial institutions, shaking the foundation of the entire financial system.

This experience remains a stark warning in U.S. financial history. It reaffirmed that the accuracy and consistency of credit reporting are directly tied to the stability of the financial system. However, these credit risks did not end in the past.

As of 2025, total U.S. credit card debt has surpassed a record $1.17 trillion, with credit card delinquency rates reaching their highest levels since 2008. Low-income households, in particular, are facing extreme financial stress, with savings rates approaching 0%.

Moreover, policy changes under the new Trump administration in 2025 have introduced another inflection point in the credit landscape. The recently passed tax reform—dubbed the “One Big Beautiful Bill Act”—eliminated income-based repayment for student loans and tightened Pell Grant eligibility for low-income students. Since student loan repayments resumed, approximately 2.2 million borrowers have experienced credit score drops of 100 points or more, with over 1 million seeing declines of 150 points or greater.

At the same time, significant cuts to Medicaid and SNAP budgets, along with stricter eligibility requirements, have increased financial insecurity among low-income households. These policy shifts are directly affecting individual credit histories and serving as indirect risk factors in financial markets. The tax reform, projected to add over $3 trillion to the deficit, triggered bond market volatility—with 30-year Treasury yields breaking above 5% for the first time in 18 months—raising alarms among Wall Street experts about broader economic impacts.

In the midst of recurring crises and policy uncertainty, there is one benchmark that both consumers and financial institutions rely on: the FICO score. Fair Isaac Corporation (FICO) is the de facto credit scoring standard used by over 90% of major U.S. lenders. Controlling 90–95% of the U.S. credit scoring market, FICO has become the gatekeeper that determines access to financial services.

Now, leveraging this unrivaled market position and its central role in the U.S. financial infrastructure, let’s take a deep dive into FICO—who they are and how they came to hold this pivotal status.

👀 Why This Company? (3‑line Summary)

1️⃣ Rising U.S. debt, soaring delinquency rates, student loan policy changes, and the Trump administration’s reforms have intensified credit risk, creating strong demand for advanced risk management and decision systems among financial institutions.

2️⃣ In this environment, FICO’s ubiquitous FICO Score and intelligent decision-making platform have positioned the company as a cornerstone of U.S. financial infrastructure.

3️⃣ With continuous shocks to credit conditions and a broader digital shift, FICO—as a provider of “decision infrastructure”—warrants renewed consideration for long-term investment.

1. Company Overview

Fair Isaac Corporation (commonly known as FICO) is an American data analytics company founded in 1956 by engineer Bill Fair and mathematician Earl Isaac. The two met at the Stanford Research Institute in Menlo Park, California, where they developed the concept for a credit scoring model. To bring their idea to market, they launched the company under the name Fair, Isaac and Company.

Today, FICO is headquartered in Bozeman, Montana, and operates in over 25 countries with approximately 3,500 employees worldwide. The company is best known for its FICO® Score, a widely used consumer credit scoring system. In addition to credit scoring, FICO supports businesses with predictive analytics, decision automation, and data science solutions that enhance decision-making efficiency.

FICO’s business is divided into two main segments. The first is the “Scores” segment, which provides credit scoring services primarily to financial institutions. The second is the “Software” segment, offering analytics and decision management software designed to automate and optimize operations across various industries. Key clients include banks, insurance companies, retailers, healthcare providers, and government agencies.

FICO’s technology is used by more than 75% of top U.S. financial institutions and by 7 of the top 10 Fortune 500 companies, reflecting its broad application across industries. The company holds more than 200 U.S. and international patents and leverages this intellectual property to help clients increase profitability, improve customer satisfaction, and achieve sustainable growth. FICO currently has a market capitalization of approximately $42 billion.

2. Key Products and Services

FICO provides differentiated solutions in the global market through its two core business segments: Scores and Software.

A. Scores Segment

a. FICO® Score (B2B Services for Enterprises)

The FICO® Score is a widely used credit scoring model that evaluates a consumer’s credit risk on a scale from 300 to 850.

It is used by 90% of top financial institutions in the U.S. as a standard in lending decisions, especially functioning as a de facto benchmark in the mortgage industry.

More recently, the FICO Score 10 T version has been adopted in the non-GSE (Government-Sponsored Enterprise) mortgage market, powering over $241 billion in annual mortgage originations and supporting portfolios exceeding $1.33 trillion in value.

FICO continues to enhance its tools with innovations such as the Mortgage Simulator, which models the impact of credit events on consumer scores.

b. myFICO.com (B2C Services for Consumers)

myFICO.com is the official platform through which consumers can directly access their FICO scores and utilize credit monitoring services.

It provides integrated scores from all three major credit bureaus—Experian, Equifax, and TransUnion—and offers tailored information through various subscription models (Basic, Advanced, Premier).

However, in FY 2024, revenue from paid web-based subscriptions declined by 2%, partly due to the U.S. government’s expansion of free credit report access.

While FICO maintains dominant market share and growth in the B2B sector, its direct revenue contribution from B2C services remains limited amid the spread of free alternatives.

B. Software Segment

a. FICO® Platform (Core Analytics and Decision Software)

The FICO Platform is a modular software solution designed to integrate advanced analytics, machine learning, and AI-driven decision-making into enterprise workflows.

It is currently deployed at over 140 financial institutions worldwide, supporting agile, data-driven decisions and enhancing customer experiences.

Through its “land and expand” strategy, FICO encourages customers to broaden their usage over time, increasing revenue per customer.

As of FY 2024, the platform's Annual Recurring Revenue (ARR) grew by 31% year-over-year.

For more details on Annual Recurring Revenue, click here.

b. Fraud Detection & Prevention

Through solutions like FICO Falcon Fraud Manager, the company offers real-time card fraud detection, application fraud prevention, and scam protection.

These tools utilize AI and machine learning-based models, and FICO holds more than 100 AI/ML patents related to fraud prevention.

The Falcon Intelligence Network enables over 10,000 financial institutions to participate in a shared intelligence framework that protects over 4 billion transactions annually.

c. Customer Lifecycle Management

FICO provides solutions that span the entire customer lifecycle—from acquisition and onboarding to account management, collections, and marketing.

Key offerings include Customer Acquisition, Originations, Collections & Recovery, and Pricing Optimization, all powered by automated analytics and decision engines to maximize operational efficiency.

For example, telecom companies use FICO solutions to automate delinquent account management and reduce customer churn simultaneously.

d. Decision Management Software

Solutions like Blaze Advisor, Xpress Optimization, and Decision Optimizer help enterprises implement complex rule-based decisions and optimization scenarios.

These tools enable fast, consistent strategic planning and drive profitability and efficiency across various industry environments.

e. Financial Inclusion Initiative

FICO is actively pursuing global initiatives aimed at expanding financial inclusion by developing alternative scoring models for individuals with limited or no credit history.

This effort enhances credit accessibility for underbanked populations and emerging markets, while strengthening partnerships with public policy organizations and financial institutions around the world.

3. Business Model

FICO has built a dual-revenue structure that combines high profitability and growth through its two core pillars: the credit scoring platform (Scores segment) and the decision management software platform (Software segment).

A. Scores Segment: Platform-Based Revenue Model as Credit Evaluation Infrastructure

a. How It Works

FICO licenses its proprietary credit scoring algorithm (FICO Score) to the three major credit bureaus in the United States—Experian, Equifax, and TransUnion.

When financial institutions (lenders) need to make decisions on loans, credit card issuance, or risk assessments, they request a consumer’s FICO Score from these bureaus.

The credit bureaus calculate the score based on FICO’s algorithm and deliver it to the lenders. A portion of the resulting revenue is paid to FICO as a royalty.

Consumers do not pay directly for their scores, but the cost is indirectly included in fees such as the “Credit Report Fee” or “Loan Origination Fee.”

Through this structure, FICO operates an automated revenue generation mechanism that scales with the volume of financial transactions—without needing direct contact with consumers.

Image Description:

This infographic visualizes the revenue model of FICO's credit scoring business.

- FICO develops the credit scoring algorithm.

- It licenses the algorithm to credit bureaus such as Experian, Equifax, and TransUnion.

- Lenders—banks, credit card companies, and loan providers—use the score to evaluate consumer creditworthiness.

- Consumers indirectly pay for the use of the score through loan-related fees.

💰 Revenue Flow Summary:

Consumer → Lender ↔ Credit Bureau → FICO

(Indirect Fee → Score Access Fee → License Royalty)

b. Revenue Model

FICO earns royalties ranging from approximately $0.20 to $1.00 per FICO Score query. In the U.S. alone, billions of credit inquiries are processed annually, generating massive cumulative revenue.

Major financial institutions typically sign annual licensing agreements instead of paying per query, using either fixed-rate or usage-based pricing structures.

On the consumer side, FICO generates B2C revenue through subscriptions to its official website (myFICO.com), which offers credit score access, credit monitoring, and identity theft protection services.

Additionally, FICO earns data distribution fees from third-party platforms such as Credit Karma and NerdWallet, creating supplementary revenue streams.

B. Software Segment: SaaS Platform for Automated Decisioning

a. How It Works

FICO offers various automated decisioning solutions to financial institutions and enterprise clients through its flagship product, the FICO Platform.

Clients can selectively use modules for fraud detection, loan underwriting automation, customer segmentation, collections, marketing optimization, and more.

The platform is cloud-based and integrates into the client’s internal data flows and systems post-implementation, encouraging continued usage and expansion.

FICO employs a “Land and Expand” strategy—clients start with a limited set of functionalities, then gradually expand usage, thereby increasing revenue per client over time.

b. Revenue Model

The Software segment generates revenue through SaaS subscriptions, per-feature module licenses, usage-based pricing models, and consulting and technical services.

For example, FICO Falcon Fraud Manager generates about $0.02 per card transaction, and large financial institutions may process hundreds of millions of such transactions annually.

Clients subscribe only to the features they need, and pricing varies depending on usage volume and number of users.

High-value professional services—such as consulting, data analytics, and model development—are offered separately for an additional fee.

As of 2024, the Software segment’s Annual Recurring Revenue (ARR) reached approximately $227 million, marking a 31% increase from the previous year, driven by high customer retention and scalable feature expansion.

4. Financial Performance

FICO has maintained consistent performance growth over the past three fiscal years and is targeting double-digit growth for FY2025. Both the Scores and Software segments remain highly profitable, and the company continues to demonstrate outstanding cash flow and capital efficiency.

A. Summary of Key Financial Metrics

FICO has shown stable growth in total revenue, net income, and earnings per share (EPS) from FY2022 to FY2025E.

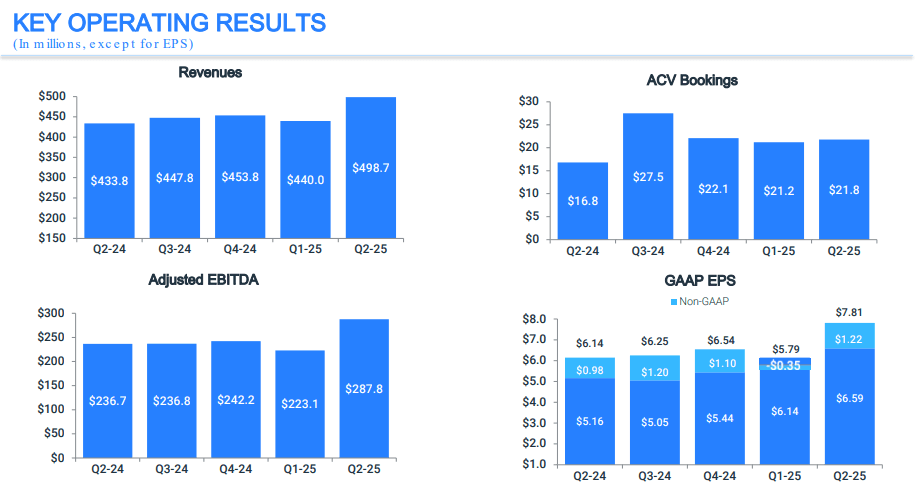

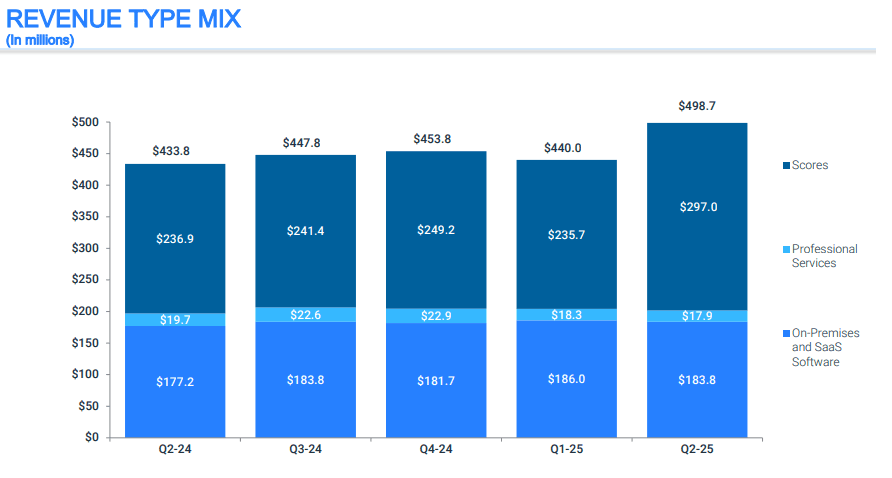

Source: FICO Investor Relations, Q2 2025 IR Presentation

Source: FICO Investor Relations, Q2 2025 IR Presentation

| Category | FY2022 | FY2023 | FY2024 | FY2025E |

|---|---|---|---|---|

| Total Revenue ($M) | 1,377.3 | 1,513.6 | 1,717.5 | 1,980.0 |

| GAAP Net Income ($M) | 373.5 | 429.4 | 513.0 | 624.0 |

| Diluted EPS ($) | ~14.56 | 16.93 | 20.77 | 25.05 |

In FY2024, total revenue increased 13% year-over-year, net income rose 19%, and EPS grew 21% to $20.77. For FY2025, the company projects $1.98 billion in revenue and $624 million in net income.

B. Segment Performance Breakdown

Source: FICO Investor Relations, Q2 2025 IR Presentation

Source: FICO Investor Relations, Q2 2025 IR Presentation

a. Scores Segment

The Scores segment generated $920 million in revenue in FY2024, representing a 19% year-over-year increase.

This growth was primarily driven by a 27% increase in B2B (financial institutions) revenue, thanks to higher pricing. In contrast, B2C (consumer-facing) revenue declined 2% due to lower transaction volume.

b. Software Segment

Software revenue reached $798 million in FY2024, growing 8% from the previous year.

Notably, Annual Recurring Revenue (ARR) from the cloud-based FICO Platform reached $227 million, up 31% year-over-year, acting as the main driver of growth in this segment.

The segment also reported a DBNRR (Dollar-Based Net Revenue Retention) of 110%, indicating strong customer retention.

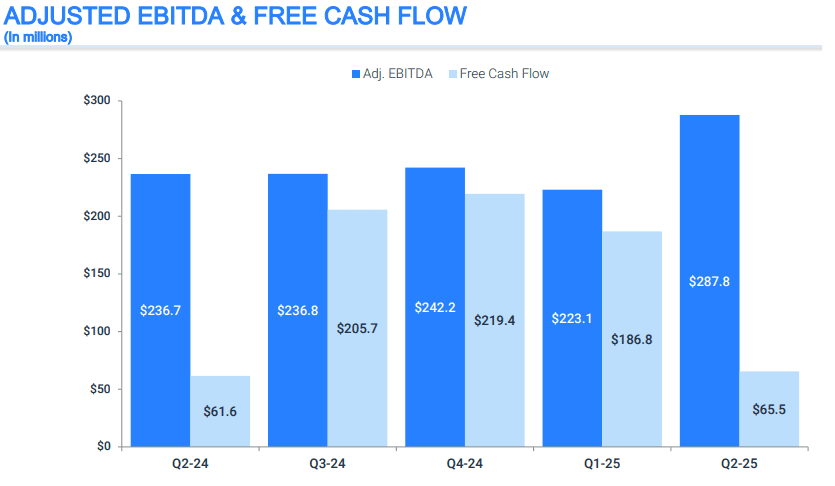

C. EBITDA and Free Cash Flow (FCF)

FICO maintains strong cash flow backed by high profitability. Over the past five quarters, both EBITDA and FCF have steadily increased, with EBITDA margins in the range of 43–45%, signaling robust profitability.

Source: FICO Investor Relations, Q2 2025 IR Presentation

Source: FICO Investor Relations, Q2 2025 IR Presentation

| Quarter | EBITDA ($M) | Free Cash Flow ($M) |

|---|---|---|

| Q1 FY2024 | 176.4 | 147.2 |

| Q2 FY2024 | 182.3 | 153.9 |

| Q3 FY2024 | 188.5 | 160.2 |

| Q4 FY2024 | 193.7 | 169.5 |

| Q1 FY2025 | 205.1 | 178.6 |

Total free cash flow in FY2024 reached approximately $607 million, providing a solid foundation for shareholder return initiatives such as share buybacks.

D. ROIC (Return on Invested Capital) Analysis

FICO achieved an exceptionally high ROIC of 45.43% in FY2024, demonstrating superior capital efficiency. ROIC is a key indicator that shows how effectively a company generates returns from its invested capital and is crucial for assessing long-term profitability and sustainability.

a. ROIC Calculation Overview

- Operating Income: $733.6M

- Effective Tax Rate: 20.1%

- Net Operating Profit After Tax (NOPAT):

$733.6M × (1 - 0.201) = $586.1M - Invested Capital:

Total Debt: $2,252.9M + Shareholders’ Equity: -$962.7M = $1,290.2M - ROIC Formula:

$586.1M ÷ $1,290.2M = 45.43%

This figure shows that FICO is generating a very high return on capital invested in the business. Typically, an ROIC above 15% is considered excellent—FICO significantly exceeds this benchmark.

b. Structural Interpretation

FICO’s exceptional ROIC is attributed to the following structural characteristics:

- Proprietary Business Model: The FICO Score has been adopted as a standard across the U.S. financial sector, creating strong market dominance and repeat demand from lenders.

- Share Buyback Strategy: Ongoing buybacks have enhanced per-share value. As a result, the company’s equity appears negative in accounting terms, though this has no adverse effect on business operations or financial health.

- Intangible Asset-Centric Structure: FICO’s algorithm- and software-driven, fixed-cost-heavy business model allows for high returns with minimal capital investment.

c. Summary

| Metric | FY2024 |

|---|---|

| Operating Income | $733.6M |

| Net Operating Profit After Tax (NOPAT) | $586.1M |

| Invested Capital | $1,290.2M |

| ROIC | 45.43% |

5. Strategy Summary: Long-Term Accumulation Perspective

A. Why This Stock Is a Long-Term Investment

FICO holds a dominant position in the fields of credit information and decision automation solutions.

The FICO® Score has become the de facto standard for credit underwriting among major U.S. financial institutions, creating recurring demand and high barriers to entry. In addition, the cloud-based FICO Platform is experiencing strong growth in the analytics automation market, supported by scalable customer expansion and a high net retention rate of 123%, solidifying a long-term revenue base.

Its business structure is built around intangible assets with fixed cost leverage, offering exceptional capital efficiency. Continuous share buybacks and a stable financial profile further strengthen its appeal for long-term holding.

B. Economic Moat

a. Types of Moats

- ✅ Intangible Assets: The FICO Score, adopted by over 90% of top U.S. financial institutions, serves as a symbol of trust, making the brand synonymous with creditworthiness.

- ✅ Network Effects: FICO's Falcon Intelligence Network, with over 10,000 financial institutions participating, increases fraud detection accuracy as more members join.

- ✅ Switching Costs: The FICO Score is embedded into core processes of lenders—such as underwriting, interest rate decisions, and regulatory reporting—making replacements costly and risky.

- ✅ Economies of Scale: FICO leverages a royalty-based algorithm model and modular SaaS platform to serve large clients at marginal incremental cost.

- ✅ Efficient Scale: The U.S. credit scoring system is essentially an oligopoly centered around FICO, with complex regulations and high client lock-in deterring new entrants.

b. Moat Rating: Wide Moat

c. Evaluation Summary

FICO possesses exceptionally strong moats in intangible assets and switching costs, effectively holding a near-monopoly in the U.S. financial ecosystem. The FICO Score is deeply embedded in mortgage and institutional lending systems, making alternatives nearly infeasible.

While network effects are partially present in fraud detection and data analytics ecosystems, the lack of direct user-to-user interaction limits their strength. Economies of scale and efficient scale are also significant, as the company spreads fixed costs across a concentrated, locked-in client base.

Potential risks include the emergence of alternatives like VantageScore and the rise of fintech-driven non-traditional credit models, which could weaken FICO’s moats over the long term.

d. Moat Reinforcement Points

| Moat Type | Reinforcement Conditions |

|---|---|

| Network Effects | Expand B2C score sharing, enhance data integration across platforms, and boost adoption of consumer apps |

| Efficient Scale | Expand internationally and increase government-level adoption, particularly in Asia and Europe (G2B) |

| Intangible Assets | Continue standardization and legal recognition through regulatory bodies and government channels |

C. Numbers-Based Summary

- 📈 Revenue CAGR +11.2% (FY2022–FY2024): Stable annual growth of about 11%, with B2B credit scoring growing even faster.

- 📈 Operating Income CAGR +16.6%: As a high fixed-cost business model, revenue growth directly translates into earnings growth.

- 📈 Diluted EPS: $20.77 (FY2024): Up 23% year-over-year, reflecting clear profitability improvement.

- 📈 ROIC: 45.4% (FY2024): Outstanding capital efficiency, demonstrating strong monopoly power and intangible asset leverage.

- 📈 FCF Margin: ~35% (FY2024): More than one-third of revenue is converted into free cash flow—indicative of strong cash generation.

- 📉 ROE is Negative (due to Share Buybacks): Not a sign of financial weakness, but rather a reflection of aggressive shareholder return policies.

- 📊 PER: ~41x (FY2024): Valuation may seem high in the short term, but the structural moat and scalability justify a long-term perspective.

- 📊 Debt-to-Equity Ratio: ~176%: The company leverages capital, but strong FCF and low interest burdens minimize financial risk.

D. Role Within a Portfolio

a. Stock Profile

FICO is a unique hybrid: a defensive player with monopoly power in credit scoring, and a growth stock driving financial institutions' digital transformation.

b. Investment Role

Within a long-term accumulation portfolio, FICO can be considered a core growth holding. Despite market volatility, its stable earnings base and steady growth can contribute to strong long-term portfolio performance.

c. Investment Strategy

Rather than reacting to short-term market noise, a disciplined accumulation approach focused on FICO's wide moat and long-term growth potential is more effective—making consistent dollar-cost averaging a suitable strategy.

E. My View and Interpretation

I view FICO as a company akin to a perpetual bond of the financial infrastructure world—its importance resurfaces whenever credit risk becomes a headline topic.

In a world where credit scores serve as the gateway to financial services, FICO stands out as an evolving platform company with both solid cash flow and technological advancement.

Its all-in-one structure—spanning digital transformation, AI, regulatory resilience, and recurring revenues—suggests that value is likely to convert into tangible results over time.

6. Competitive Advantages

FICO has maintained a leading position in the U.S. credit scoring and decision software markets for decades, driven not just by technical superiority, but by deep-rooted structural advantages across the industry.

A. Dominant Market Share and Brand Power

a. FICO Score as the De Facto Market Standard

The FICO Score has become the de facto standard in the U.S. credit evaluation market.

Approximately 75% of the top 100 U.S. financial institutions use FICO Scores for credit underwriting, and over 90% rely on FICO-based credit risk assessment tools.

Roughly 90% of all U.S. mortgage loans are based on FICO Scores, and consumers broadly associate “FICO” with “credit score.”

b. High Market Share and Switching Costs

In the mortgage industry, Fannie Mae and Freddie Mac have required FICO Scores for decades.

For financial institutions, switching to alternative models would entail substantial system rework, regulatory validation, and retraining costs—creating high switching barriers.

This structure ensures recurring revenue and strong customer lock-in for FICO.

c. Superior Position vs. Competitors

Though often grouped under "Other Fintechs" in the broader fintech space, FICO maintains a dominant share in the credit scoring niche compared to Experian, Equifax, and TransUnion.

As of 2013, over 10 billion FICO Scores had been sold to financial institutions, and more than 30 million consumers had accessed their FICO Scores directly.

B. Profitability and Pricing Power

a. Extremely High Margin Score Business

In 2024, FICO’s Score segment recorded an operating margin of 88%—a level driven by its fixed-cost software model and monopolistic market position, which is difficult for competitors to replicate.

This highly profitable Score business lifts FICO's overall operating margin (in the 40% range) and supports the company’s financial stability.

b. Recurring Revenue Through B2B Score Licensing

The FICO Score operates on a usage-based licensing model, with lenders paying per credit check.

Long-term contracts and minimum usage guarantees contribute to revenue stability, while high trust levels make price increases easily accepted.

c. Large-Scale Revenue Through High-Frequency Transactions

While the per-score fee is small, billions of credit inquiries annually in the U.S. translate into massive cumulative revenue.

This high-frequency transaction model enables recurring revenue and economies of scale, maintaining profitability while reducing price sensitivity.

d. Minimal Price Resistance Relative to Loan Size

Though lenders pay for FICO Scores, the cost is negligible in the context of loan sizes that typically exceed hundreds of thousands of dollars.

This means price hikes rarely face pushback from either financial institutions or consumers, allowing FICO to maintain pricing power.

e. Core Decision Integration Minimizes Customer Churn

FICO Scores are directly used in key financial decisions like loan approval, interest rate setting, and credit limits.

This deep integration makes switching risky—customers are more likely to view alternatives as threats to stability and compliance rather than viable options.

C. Technological Leadership and Data Expertise

a. Pioneer in AI and Predictive Modeling

With over 65 years of experience, FICO has built vast credit data assets and advanced predictive analytics capabilities.

It holds more than 200 patents, and its algorithms have been widely deployed in real-world financial systems, with the FICO Score recognized as best-in-class for practical accuracy.

b. Strategy of Augmented Intelligence

FICO takes a Responsible AI approach that prioritizes explainability and human oversight, rather than using opaque "black box" models.

This has earned trust from regulators and financial institutions—essential in highly regulated industries.

FICO’s Philosophy on Explainable AI

- FICO avoids black-box AI that lacks transparency, which often draws criticism from governments and the public.

- It develops AI systems that can clearly explain how results are produced.

- Fairness is embedded into model design to ensure no group is unfairly impacted.

- FICO promotes transparency to build confidence among clients and regulators.

This approach—termed “Augmented Intelligence”—pairs AI with human experts (e.g., data scientists, credit professionals) to co-pilot decision-making. This is a major competitive advantage in finance, where trust and compliance are paramount.

c. Scalable Infrastructure via FICO Platform

The FICO Platform integrates AI, machine learning, and real-time analytics into a smart decisioning solution.

In IDC’s 2024 MarketScape, FICO Platform was recognized as a global leader in decision intelligence platforms.

It also ranked in the Top 10 of Chartis’ RiskTech100 report in 2025, confirming its innovation and leadership.

Such endorsements serve as indirect assurance of trust and performance for enterprise clients, lowering the perceived risks of adoption.

D. Client Base, Partnerships, and Industry Standardization

a. Broad and Diversified Client Base

FICO serves over 120 countries, with clients across sectors including finance, insurance, telecommunications, retail, and government.

8 of the top 10 U.S. insurers, 300+ large retailers, and 200+ public institutions rely on FICO solutions.

b. Global Partner Ecosystem

FICO collaborates with global IT services firms like TCS and iSON Xperiences to co-develop industry-specific solutions.

Its API marketplace allows partners to seamlessly integrate with FICO’s platform infrastructure.

c. Regulatory Embedding Drives Sustainability

FICO Scores have long been adopted by U.S. regulatory bodies such as the Federal Housing Finance Agency (FHFA) as the standard for mortgage eligibility.

This regulatory embedding reduces the likelihood of replacement and ensures sustained demand.

However, shifts such as the approval of VantageScore 4.0 warrant close monitoring.

d. Persistent Institutional Trust Despite Alternatives

Though alternatives like VantageScore 4.0 are gaining regulatory approval, actual adoption by lenders remains limited.

Financial institutions, responsible for major credit decisions, tend to stick with the time-tested FICO Score due to its proven accuracy and stability.

Even with policy changes, market adoption is likely to remain conservative, favoring the established model.

e. High Customer Expansion and Retention Rates (NRR)

FICO demonstrates excellent revenue expansion within its customer base. In 2024, the dollar-based net retention rate (DBNRR) for FICO Platform customers reached 123%.

This indicates not only low churn, but also strong upsell through module upgrades and feature expansions post-initial adoption.

The overall Software segment’s NRR is around 110%, reflecting consistent revenue growth across all customer tiers.

FICO’s “Land and Expand” strategy encourages clients to start small, then scale into advanced functions like fraud detection, marketing automation, and real-time risk analysis.

E. Regulatory Environment and Industry Standardization

a. FICO Score as a Regulatory Benchmark

U.S. regulatory bodies such as the FHFA have long used the FICO Score as a benchmark for mortgage eligibility.

Many banks and lenders have aligned their internal risk models with FICO standards, creating a strong regulatory moat.

b. Regulatory Response and Adaptability

Although there are recent discussions about incorporating VantageScore 4.0, FICO has actively defended its market position through strong compliance efforts.

CEO Will Lansing views regulation as an opportunity, emphasizing FICO’s commitment to legal and technological compliance.

c. Positioning as a Compliance Enabler

FICO provides solutions like CCS (Customer Communication Services) that help clients meet regulatory requirements while improving customer experience.

This turns regulatory demands into a competitive edge rather than a risk.

7. Risk Factors

Despite its strong market share and technological leadership, FICO faces several key risks that could materially impact its long-term profitability and market dominance.

A. Intensifying Competition and Emergence of Alternatives

a. Rising Competition from VantageScore and Direct Alternatives

VantageScore—jointly developed by the three major credit bureaus (Experian, Equifax, and TransUnion)—has gained traction as a direct competitor to FICO, recently receiving formal approval from the Federal Housing Finance Agency (FHFA).

Beginning in 2025, the FHFA has allowed the use of VantageScore 4.0 for government-backed mortgages, posing a significant challenge to FICO’s monopoly position.

Some institutions, such as Synchrony Bank, have already transitioned to VantageScore. In 2024, VantageScore was used 41.7 billion times, up 55% from the previous year.

b. Growth of Fintech and Alternative Data-Based Credit Models

Fintech companies like Credit Karma and Credit Sesame are expanding their consumer bases by offering credit services using alternative data sources.

As models that incorporate non-traditional data—such as rent payments, financial app activity, and even social media—gain popularity, FICO’s traditional scoring influence could diminish.

c. Expanding Competition in the Software Segment

FICO’s decision software platform faces stiff competition from companies like Pegasystems, IBM, Adobe, Salesforce, and SAS.

Rivals offer specialized solutions in fraud detection, loan underwriting, and marketing automation, adding pressure on pricing, features, and distribution channels.

B. Rapid Technological Change and Internal Limitations

a. Accelerating AI and Machine Learning Development

Machine learning models are rapidly reshaping the credit scoring space, and major banks are increasingly developing their own in-house models based on proprietary data and algorithms.

This could reduce the need for third-party scores like FICO.

b. Data Access and Quality Risks

FICO’s predictive modeling relies heavily on credit data sourced from clients and partner institutions.

If data providers limit access due to privacy concerns, regulatory changes, or strategic shifts, it could degrade FICO’s analytics capabilities and product quality.

C. Regulatory and Legal Risks

a. Antitrust Investigations and Rising Litigation

Since 2020, FICO has faced more than 10 antitrust lawsuits filed by the U.S. Department of Justice (DOJ), financial institutions, and consumer advocacy groups.

In September 2023, a U.S. federal court allowed a case to proceed alleging that FICO inflated its score pricing, which could impact its overall pricing and distribution strategies.

In March 2024, Senator Josh Hawley requested the DOJ to reopen investigations into FICO’s market dominance and alleged price inflation practices.

b. Expansion of Regulator-Sanctioned Alternatives

Starting in 2025, the FHFA has ended the exclusive use of FICO Scores for government-guaranteed mortgages, allowing VantageScore 4.0 to be used in parallel.

This change is expected to reduce score-related revenues from the mortgage market. Future policies, such as the privatization of GSEs, could introduce additional revenue risks for FICO.

c. Rising Global Data Privacy and Compliance Burdens

FICO must comply with diverse data protection and financial IT regulations globally, including fair use of personal data, algorithm transparency, and AI bias mitigation.

Frameworks like the EU's GDPR, state-level U.S. privacy laws, and other financial security standards increase compliance costs and legal exposure.

D. Channel and Customer Concentration

a. Channel Dependency Risk

FICO Scores are distributed to financial institutions primarily via the three U.S. credit bureaus (Experian, Equifax, TransUnion), which accounted for about 45% of total revenue in 2024.

If these partners continue to strengthen their own models like VantageScore, FICO’s distribution reach could decline.

b. Industry and Geographic Concentration Risk

About 91% of FICO’s revenue comes from the financial sector, and 84% is concentrated in North America.

This makes FICO highly sensitive to macroeconomic factors such as interest rate hikes, credit contraction, and economic downturns in the U.S. financial market.

8. Future Vision and Outlook

A. Strategic Direction: Evolving into an “Intelligent Enterprise”

a. Strategic Shift Toward the FICO Platform

FICO is transitioning from a traditional data-driven credit scoring model to an intelligent decisioning platform that integrates AI and advanced analytics capabilities.

At FICO World 2025, CEO Will Lansing emphasized this direction, stating, “Only intelligent organizations—not just digital ones—will lead the future,” highlighting the critical role of the FICO Platform in transforming the company’s structure.

b. Customer Expansion via Land and Expand Strategy

FICO is actively converting on-premise software customers to the cloud-based FICO Platform and encouraging adoption across multiple departments within client organizations.

This “Land and Expand” strategy is designed to increase customer lifetime value and boost average revenue per customer.

As of 2024, the FICO Platform’s dollar-based net retention rate (DBNRR) stood at 123%, indicating that customers continue to upgrade and expand functionality post-initial adoption, driving sustained revenue growth.

c. Expanding Global Ecosystem and Technology Partnerships

FICO is accelerating its cloud platform expansion through partnerships with global tech players like AWS and TCS, and is building an open ecosystem via its API marketplace.

This strategy allows clients to integrate FICO Platform with various external solutions, enhancing flexibility and scalability.

B. Growth Across Core Business Segments

a. Market Expansion Strategy for the Scores Segment

FICO continues to roll out new models like Score 10 T and has partnered with Mortgage Capital Trading (MCT) to expand credit score usage in the mortgage market.

Additional solutions such as the Mortgage Simulator are being introduced to further increase FICO’s relevance in home financing.

b. Profitability-Focused Growth in the Software Segment

The cloud-based FICO Platform offers high-value features like real-time analytics, fraud detection, and regulatory compliance tools, making it a core enterprise decisioning system for financial institutions.

By leveraging repeatable revenue streams across diverse customer groups, FICO ensures both stability and long-term growth of its platform business.

c. Synergies Between the Two Core Segments

FICO creates integrated competitive advantages by linking its extensive credit score data assets with its software analytics capabilities.

This structure enhances customer retention, facilitates cross-selling, and maximizes profitability through expanded feature adoption.

C. Market Landscape and External Evaluations

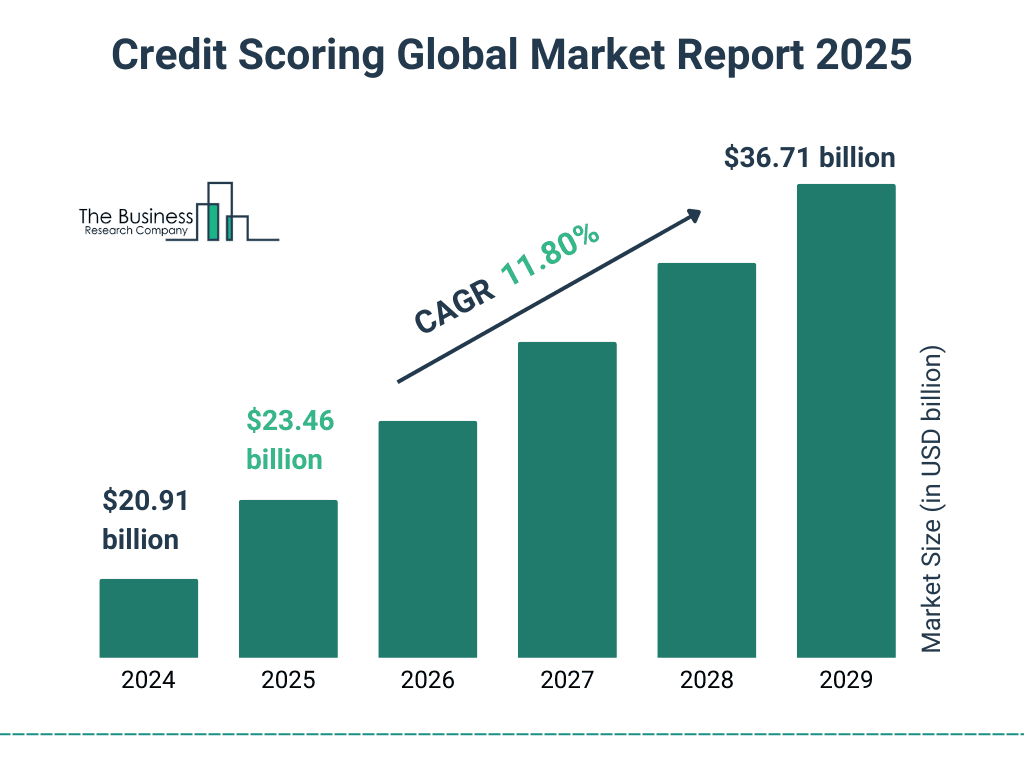

a. Structural Growth in Credit Scoring and Data Analytics Markets

- Credit Scoring Market: Projected to grow from $20.9B in 2024 to $36.7B in 2029 (CAGR 11.8%)

- Fraud Detection & Risk Analytics Market: $8.5B in 2024 → $45.2B by 2034 (CAGR 18.2%)

- Financial Services Data Analytics Market: $11.7B in 2025 → $18.2B by 2033 (CAGR 12.1%)

Source: The Business Research Company’s Credit Scoring Global Market Report 2025

Source: The Business Research Company’s Credit Scoring Global Market Report 2025

b. Positive Analyst Coverage and Investor Sentiment

Major investment firms such as Barclays and Bank of America have issued price targets ranging from $2,250 to $3,700, anticipating double-digit growth in both revenue and earnings.

Wall Street analysts also maintain a favorable outlook on FICO’s strategy and competitive position, with ratings such as “Strong Buy” and “Moderate Buy.”

c. Shareholder Returns and Financial Outlook

FICO is enhancing shareholder value through consistent share repurchases. For FY2025, the company has guided for revenue growth exceeding 15% and non-GAAP EPS growth of 25%.

With rising free cash flow, margin improvements are also expected as the platform business continues to scale.

9. Two-Minute Pitch

Peter Lynch emphasized the importance of being able to deliver a two-minute pitch about a stock you are interested in, including the reasons for buying it, the company’s prospects, and its story. If you have thoroughly researched and can confidently articulate this two-minute pitch, you may consider purchasing the stock.

(Note: All investment decisions and responsibilities rest solely with you. Always invest with surplus funds and focus on long-term investments.)

Founded in 1956 by Bill Fair and Earl Isaac, FICO began as a visionary credit scoring model and has since grown into a global enterprise with offices in over 25 countries. Today, FICO goes far beyond providing credit scores—it delivers predictive analytics and data science solutions that support intelligent decision-making across industries worldwide.

The company’s core operations are divided into two main segments: Scores and Software. The FICO® Score has become the de facto standard for over 90% of U.S. financial institutions in credit underwriting, especially prominent in the mortgage industry. FICO continues to enhance its market leadership through ongoing model innovation. Meanwhile, the Software segment, powered by the FICO Platform, offers solutions for fraud detection, customer lifecycle management, and automated decision-making. The platform demonstrated strong momentum, with Annual Recurring Revenue (ARR) growing by 31% in the most recent fiscal year.

FICO’s dual-revenue model—platform-based royalty income from the Scores segment and SaaS subscription revenue from the Software segment—enables the company to sustain both profitability and growth. This resilient model is reflected in its financial performance: in FY2024, FICO posted 13% revenue growth and 19% net income growth. With an EBITDA margin of 45% and an outstanding Return on Invested Capital (ROIC) of 45.43%, FICO proves its ability to generate returns with exceptional capital efficiency.

Of course, challenges remain—including the rise of alternative models like VantageScore, intensifying fintech competition, and evolving regulatory risks. However, FICO is well-positioned to navigate these threats, supported by its dominant market share, brand power, and an 88% operating margin in the Scores business. Its technological leadership in AI and predictive modeling further strengthens its moat. Notably, FICO promotes “Augmented Intelligence,” a responsible AI framework that combines transparency, fairness, and human oversight—earning the trust of financial institutions and regulators alike.

FICO’s vision is to evolve into an “Intelligent Enterprise.” With its “Land and Expand” strategy centered around the FICO Platform, the company is increasing customer lifetime value and expanding its footprint within existing clients. Its 123% net revenue retention (NRR) illustrates robust growth from its current customer base. At the same time, the structural growth of the global credit scoring and data analytics market continues to provide a favorable tailwind for FICO’s future.

With market dominance, best-in-class profitability, and continuous innovation, FICO delivers long-term value and reliability for any investor’s portfolio. It is not merely a credit scoring company—it is a next-generation platform enterprise shaping the future of intelligent decision-making through data and AI.