Outlook for the U.S. Robotics Industry in 2025–2026 and Analysis of Promising Stocks

1. Introduction: The Arrival of Physical AI and a Structural Reshaping of the Market

By late 2025, the global robotics industry has reached an unprecedented structural turning point. If capital markets spent the past several years focused on Generative AI and semiconductor infrastructure, that focus is now shifting rapidly toward Physical AI—where intelligence is fused with a physical form to control the real world. This is not a simple sector rotation; it signals that the technological convergence of IT (Information Technology) and OT (Operational Technology) is entering a mature, execution-ready phase.

A definitive signal of this paradigm shift is SoftBank Group’s agreement in October 2025 to acquire Swiss ABB’s robotics business for approximately $5.4 billion. This suggests that large-scale capital is beginning to revalue the robotics "installed base" not merely as machinery, but as a core platform for deploying AI software and collecting real-world data.

This report provides an in-depth analysis of promising companies across Japan and Europe—markets that operate outside the software-centered U.S. ecosystem yet dominate the physical engineering landscape. These regions remain strongholds of precision manufacturing, hardware engineering, and system integration. Our analysis is based on financial data from the second half of 2025 and real-world order trends, focusing on capturing investment opportunities driven by shifts in the global value chain.

2. Objective and Methodology

This report is designed for investors considering global robotics-themed investments outside the United States. While the U.S. leads in AI software, the precision manufacturing technologies that build the robot’s “body” and “joints” are still dominated by Japan and Europe.

To understand global capital flows, we dissected the portfolios of major U.S.-listed robotics ETFs. By analyzing where their non-U.S. allocation is concentrated, we identify “core non-U.S. contenders” grounded in institutional capital deployment (smart money) rather than theme-driven hype.

The primary ETFs analyzed are:

- BOTZ (Global X Robotics & Artificial Intelligence ETF): Large-cap focused, weighted toward market cap. It holds high exposure to Japan’s major robotics manufacturers such as Fanuc and Keyence.

- ROBO (ROBO Global Robotics and Automation Index ETF): Prefers an equal-weight approach across the value chain. It is optimized for identifying “hidden champion” component leaders in Europe and Japan.

- ARKQ (ARK Autonomous Technology & Robotics ETF): Concentrates on disruptive innovators. It includes select Japanese/European companies involved in autonomous technologies.

By extracting overlapping holdings across these ETFs, we derived a set of consensus picks chosen by multiple asset managers.

3. Analytical Framework: Viewing the Market Through Institutional Eyes

Analyzing how global robotics ETFs allocate to Non-U.S. companies is key to understanding the market’s underlying structure.

A. How Major Global ETFs Approach the Non-U.S. Market

BOTZ (“Manufacturing Kingpins”):

Excluding U.S. giants like NVIDIA, BOTZ places its largest weight on Japan’s precision manufacturing leaders. It treats ABB (now acquired by SoftBank), Fanuc, and Yaskawa Electric—the “traditional Big 4” of industrial robots—as core assets, operating under the view that factory automation cannot function without them.

ROBO (“Core Components and European Engineering”):

ROBO focuses not only on finished robots but also on critical components such as reducers and sensors. Harmonic Drive (Japan) and Siemens (Germany) rank among its top holdings, implying that robotics growth directly translates into earnings power for component suppliers and Systems Integrators (SI).

ARKQ (“Disruptive Innovation”):

While heavily U.S.-focused, ARKQ selectively picks non-U.S. companies that enable autonomy, such as Komatsu (autonomous mining) or specific drone technology firms, validating their technological moats.

B. Deriving “Core Non-U.S. Consensus Picks” Through Cross-Validation

The following Non-U.S. consensus list was selected through ETF overlap analysis. These are validated companies that hold meaningful top-weight positions in at least two major ETFs.

| Category | Core Company (Ticker) | Key ETFs | Investment Thesis Summary |

|---|---|---|---|

| Game Changer | SoftBank Group (9984) | BOTZ, ROBO | Secures hardware leadership via ABB Robotics acquisition. |

| Manufacturing / OEM | Fanuc (6954) | BOTZ, ROBO | Global #1 in industrial robots; beneficiary of U.S. Capex cycle. |

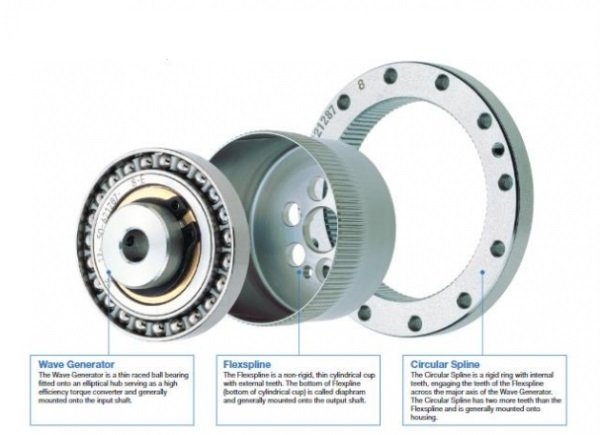

| Core Components | Harmonic Drive (6324) | ROBO | Near-monopoly position in humanoid joints (precision reducers). |

| Sensors / Vision | Keyence (6861) | BOTZ | Ultra-high-margin sensor & machine-vision leader (~50% op margin). |

| Control / Software | Yaskawa Electric (6506) | ROBO, BOTZ | Leader in motion control (servo motors); expanding NVIDIA partnership. |

| Systems / SI | Siemens (SIE) | ROBO | Leader in industrial metaverse and digital-twin platforms. |

4. Deep Dive: Macro and Industry Themes

A. The SoftBank–ABB Mega-Deal: Higher Capital Intensity and a Valuation Re-Rating

SoftBank’s acquisition of ABB’s robotics business announced in October 2025 ($5.375B) is a milestone that resets how the market values hardware robotics manufacturers. While ABB previously focused on electrification and automation for efficiency, SoftBank has signaled a strategy to combine ABB’s installed base of 400,000+ robots with its own AI semiconductor and logistics technologies—turning that footprint into a global data interface.

The implications are clear: Robotics hardware is transforming into a capital-intensive industry where survival requires the combination of massive capital and advanced AI capabilities. Incumbent leaders like Fanuc and Yaskawa Electric now face pressure to accelerate collaboration with Big Tech or drastically strengthen their software capabilities. Yaskawa’s intensified cooperation with NVIDIA is a direct response to this trend.

B. Regional Demand Decoupling and the 2026 Outlook

After robot shipments declined amid the 2024 slowdown, recovery has started to diverge sharply by region in the second half of 2025. Investors should monitor this decoupling dynamic.

- North America: The primary growth engine for Japanese and European robot makers. Driven by labor shortages and reshoring policies, Japan’s machine tool orders to the U.S. rose for two consecutive months in September 2025 (recovering to around ¥30B). This serves as a leading indicator that U.S. manufacturing Capex is restarting.

- China: The era of explosive infrastructure investment has cooled, but qualitative change is evident. Automation demand remains resilient in the “new three” industries—EVs, batteries, and solar. However, the rise of local Chinese players is forcing foreign companies to move further upmarket into high-end segments.

- Europe: The slowest region to recover. Weak German manufacturing has suppressed robotics import demand. However, regulations on energy efficiency and Digital Transformation (DX) are creating opportunities for software and SI leaders like Siemens.

C. The End of Destocking and the Rise of Humanoids

Crucially, the excess inventory problem that pressured the industry in 2023–2024 has entered a resolution phase in late 2025. Key component makers such as Harmonic Drive Systems have reported that inventory adjustments are largely complete.

Even more notable is the opening of the humanoid robotics market. Harmonic Drive’s humanoid-related orders in Q2 2025 reached ¥1.3 billion, with growth expected to increase 2–3x by 2027. This suggests humanoids are moving beyond the lab into pilot production for commercialization.

| Category | Status in 2H 2025 | 2026 Outlook | Key Drivers |

|---|---|---|---|

| Inventory Cycle | Late-stage destocking | Restocking begins | U.S. rate cuts, Capex recovery |

| Key Markets | North America strong; selective China recovery | North America expansion continues; India emerges | Reshoring, supply-chain diversification |

| Tech Trends | Collaborative robots (cobots) spreading | Humanoid prototype competition accelerates | AI convergence, labor substitution |

5. Japan: The Fortress of Precision Manufacturing and Hardware

Japan remains the manufacturing heart of global industrial robotics, accounting for roughly 47% of the global market. With SoftBank’s entry, the dynamism of the Japanese market has intensified.

A. SoftBank Group (9984.T / SFTBY) — The New Robotics Powerhouse

Company Overview and Acquisition Impact:

Company Overview and Acquisition Impact:

Through the acquisition of ABB’s robotics business, SoftBank instantly becomes a major global player in robotics hardware. Moving beyond indirect exposure via its Vision Fund, it now directly secures a global infrastructure base of 400,000+ robots.

Core Synergies:

The assets SoftBank gains include ABB’s multi-joint industrial robots (IRB series) and its collaborative robot (cobot) technology, YuMi. These hardware platforms are expected to integrate with high-performance chips from Arm (a SoftBank subsidiary) and advanced AI autonomous models.

Investment Strategy:

For investors who previously looked to ABB for robotics exposure, SoftBank Group is now the alternative. The stock is positioned to reflect both robotics hardware revenue and the value of the AI software layer.

B. Fanuc (6954.T / FANUY) — Global No.1 in Industrial Robots

Current Position:

Current Position:

Fanuc is the global market-share leader in CNC systems and industrial robots. Known for its high degree of in-house component production, it maintains a stable and resilient profit structure.

Outlook:

Fanuc is a prime beneficiary of the U.S. Capex cycle. Analysts expect a recovery in factory automation demand in 2026, driven by the expansion of its cobot lineup and a sustained operating margin in the 20%+ range.

C. Yaskawa Electric (6506.T / YASKY) — Leader in Motion Control

Current Position:

Current Position:

Yaskawa is a dominator in the servo motor market—the critical "muscle" for robot actuation.

Outlook:

The company is accelerating intelligent robot development through an expanding collaboration with NVIDIA. Despite intensifying competition from local Chinese players, Yaskawa maintains its edge in high-precision control technologies, with improving profitability confirmed in 2025.

D. Harmonic Drive Systems (6324.T / HSYLF) — The "Joints" of Humanoids

Current Position:

Current Position:

Harmonic Drive holds world-class capabilities in precision reducers (strain wave gears), which are essential for the movement of robotic joints.

Outlook:

Humanoid robots require significantly more reducers per unit than conventional industrial robots. This positions Harmonic Drive as a direct beneficiary of unit volume (Q) expansion. The recent surge in humanoid-related orders provides tangible support for future earnings growth.

E. Keyence (6861.T / KYCCF) & SMC (6273.T / SMCAY) — High-Margin Leaders

Keyence: A fabless leader in factory automation sensors and machine vision, consistently delivering operating margins above 50%. It is a key beneficiary of advanced manufacturing facility buildouts in the U.S.

SMC: The global leader in pneumatics technology. Earnings improvement is expected as the semiconductor equipment market enters a recovery cycle.

6. Europe: Industrial Software and Systems Integration

With ABB Robotics hardware shifting to SoftBank, the European opportunity is increasingly defined by software and systems integration (SI).

A. Siemens (SIE.DE / SIEGY) — Industrial Software and Digital Twins

Current Position:

Siemens holds dual capabilities in hardware control (PLCs) and virtual factory software (Digital Twin).

Outlook:

Its “Industrial Metaverse,” developed in collaboration with NVIDIA, is becoming a standard platform for simulating robot deployments before physical installation. The company’s strength lies in a recurring-revenue model with higher margins than pure hardware sales.

B. AutoStore (AUTO.OL / AUTOY) — High-Density Warehouse Automation

Current Position:

Current Position:

AutoStore’s “cube storage” system maximizes space efficiency in warehouse automation, supported by a highly profitable structure with gross margins around 73%.

Outlook:

Continued e-commerce growth and space constraints in urban fulfillment centers drive sustained demand. A robust backlog provides a solid foundation for growth heading into 2026.

7. Conclusion: Investment Strategy and Key Takeaways

A. Integrated Investment Strategy

Looking ahead to 2026, the non-U.S. robotics market faces two powerful tailwinds: the practical implementation of Physical AI and the reshoring-driven investment cycle. Investors should consider a diversified approach:

- The Game Changer: SoftBank Group. By acquiring ABB’s robotics business, SoftBank is integrating AI capabilities with massive hardware scale—making it the central player in the market’s reshaping.

- Core Holdings: Fanuc and Keyence. These are the "picks and shovels" of the U.S. manufacturing rebound, supported by pristine balance sheets.

- High Growth: Harmonic Drive and Yaskawa Electric. These offer direct exposure to the humanoid robotics boom and deeper AI convergence.

- Digital Platform: Siemens and AutoStore. Ideal for investors preferring high-margin, software-driven business models over pure hardware.

B. Final Summary

The strategic shifts in 2025 signal that robots are evolving from standalone machines into intelligent data platforms. As we move into 2026, hardware companies that successfully attach AI at scale will see accelerated earnings growth. Beyond individual hardware names, investors should pay close attention to platform players—like SoftBank and Siemens—that have the power to orchestrate this broader ecosystem.